Indian startups face a critical funding gap as Series C and later rounds collapse by 27% year-over-year, stranding companies in the 'missing middle' between early promise and sustainable scale. The retreat of global giants like Tiger Global and SoftBank, coupled with brutal valuation markdowns and failed IPOs, forces founders into survival mode. Without urgent solutions to rebuild growth capital and exit pathways, India risks an ecosystem that births innovators but fails to mature them into endu

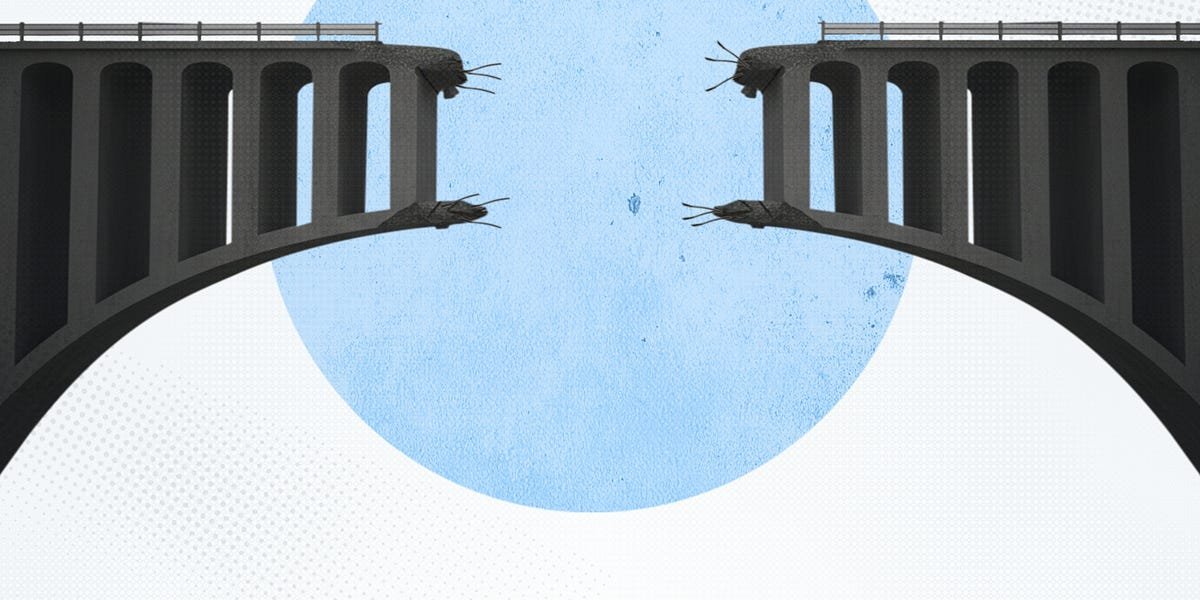

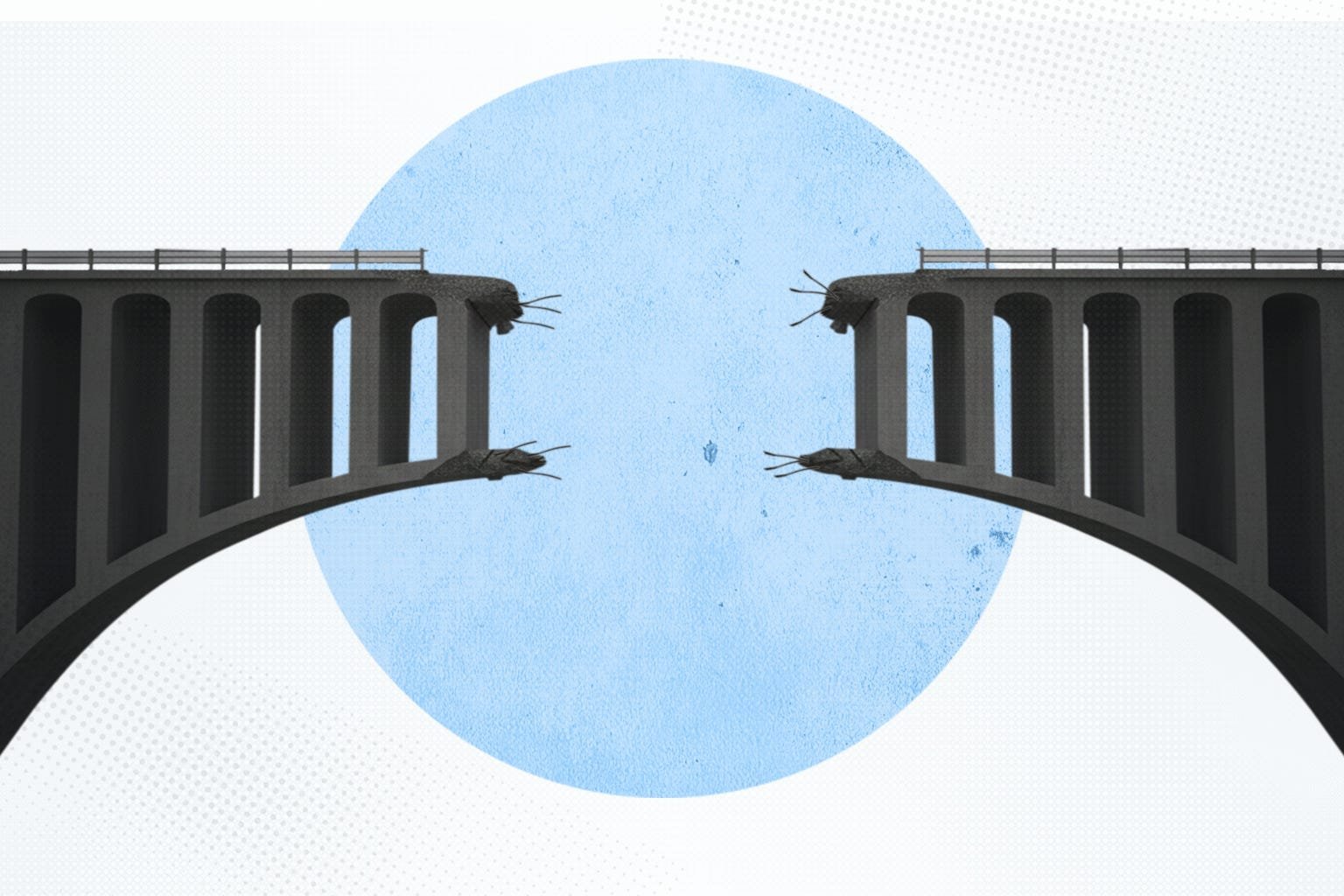

A healthy venture capital ecosystem resembles a relay race: capital passes seamlessly from seed to Series A, B, C, and beyond, ultimately crossing the finish line via IPO or acquisition. In India today, the baton is being dropped at the most critical leg – the growth stage. While early-stage funding remains robust and the aspiration of IPOs persists, Series C and later rounds have collapsed by 27% year-over-year in the first half of 2025, creating a dangerous void where startups need capital most to prove they can scale sustainably. This "missing middle" is forcing founders into impossible choices: shelving global ambitions, delaying expansion, or chasing premature profitability just to survive.

The Numbers Tell the Story:

- H1 2025 Indian Tech Funding: $4.8 billion (down 25% YoY)

- Late-Stage Contribution: $2.7 billion (down 27% YoY)

- Growth Stage Suffering: Series C+ rounds hardest hit, despite representing peak capital needs.

The retreat of global crossover funds is a primary driver. Tiger Global, Sequoia (now Peak XV Partners), and SoftBank – once the engines of India's late-stage growth with $50-$100 million cheques – have dramatically pulled back. Tiger focuses on defending existing portfolios, Peak XV downsized its growth fund by nearly $500 million during its split, and SoftBank, scarred by losses in Oyo, Ola, and Paytm, has retreated decisively. Domestic funds lack the scale to fill this chasm.

Why the Growth Stage Stalemate?

- Valuation Hangover: The exuberant 2020-22 period saw growth rounds priced for "tripling revenues annually." Reality bit hard, leading to brutal 70-80% markdowns for giants like Byju's and PharmEasy. Investors now see systemic overpricing risk.

- IPO Disillusionment: Landmark listings like Zomato, Nykaa, and Paytm plunged 40-70% post-IPO. This shattered confidence in bridging private-market optimism with public-market discipline, making late-stage underwriting nearly impossible.

- Exit Drought: Only three $500M+ tech IPOs occurred in 2024 vs. twenty+ in 2021/22. Billion-dollar acquisitions are rare. Without viable exits, late-stage capital becomes "bridge financing with no bridge."

- Governance Erosion: Scandals in edtech, mass layoffs, and fintech accounting lapses further eroded investor confidence in backing complex, scaling entities.

The M&A Mirage: While acquisitions could theoretically recycle capital, India's M&A market is underdeveloped. Tech accounted for less than 4% of India's H1 2025 $50B deal value, starkly contrasting with 25-33% in the US/Europe. Key barriers include:

- Few profitable targets for strategic buyers.

- Corporates wary of integration risks.

- Regulatory friction around foreign investment and taxation.

- Founder mindset viewing acquisition as failure, not strategy.

Rebuilding the Middle: Possible Pathways Despite the gloom, solutions exist but require coordinated effort:

- Dedicated Growth Vehicles: Sovereign wealth funds, pensions, and insurers must back stage-specific funds with patient capital.

- Corporate Acquisition Incentives: Policy and cultural shifts encouraging corporates to acquire for tech/IP/talent, not just revenue.

- Regulatory Streamlining: Simplifying share transfers and foreign investment procedures to accelerate deals.

- IPO Framework Reform: Creating pathways for high-growth, pre-profitability companies to list realistically.

The Series C+ crunch exposes the fragility of India's venture ecosystem. Startups are caught between the fading narrative-driven optimism of early stages and the harsh discipline of public markets, amplified by past excesses and governance lapses. Without rebuilding the pools of growth capital and the pathways to liquidity, India risks becoming a nursery for startups that never grow into the enduring tech champions its economy desperately needs. The relay baton must be passed, or the race cannot be won.

Source: DealflowIQ & Deshna Jain, 'The Missing Middle' (Oct 02, 2025)

Comments

Please log in or register to join the discussion