Intel has discontinued its Software Defined Silicon (SDSi) program after archiving its GitHub repository and removing documentation, signaling the end of efforts to monetize disabled accelerators in Xeon processors through post-purchase activation.

Intel has officially halted development of its Software Defined Silicon (SDSi) initiative, marking the quiet demise of a controversial four-year effort to monetize disabled hardware accelerators in Xeon server processors. The program’s GitHub repository was archived in November 2025, while Intel simultaneously scrubbed most documentation from its official channels. This coordinated withdrawal signals strategic abandonment ahead of next-generation Xeon 6 platforms.

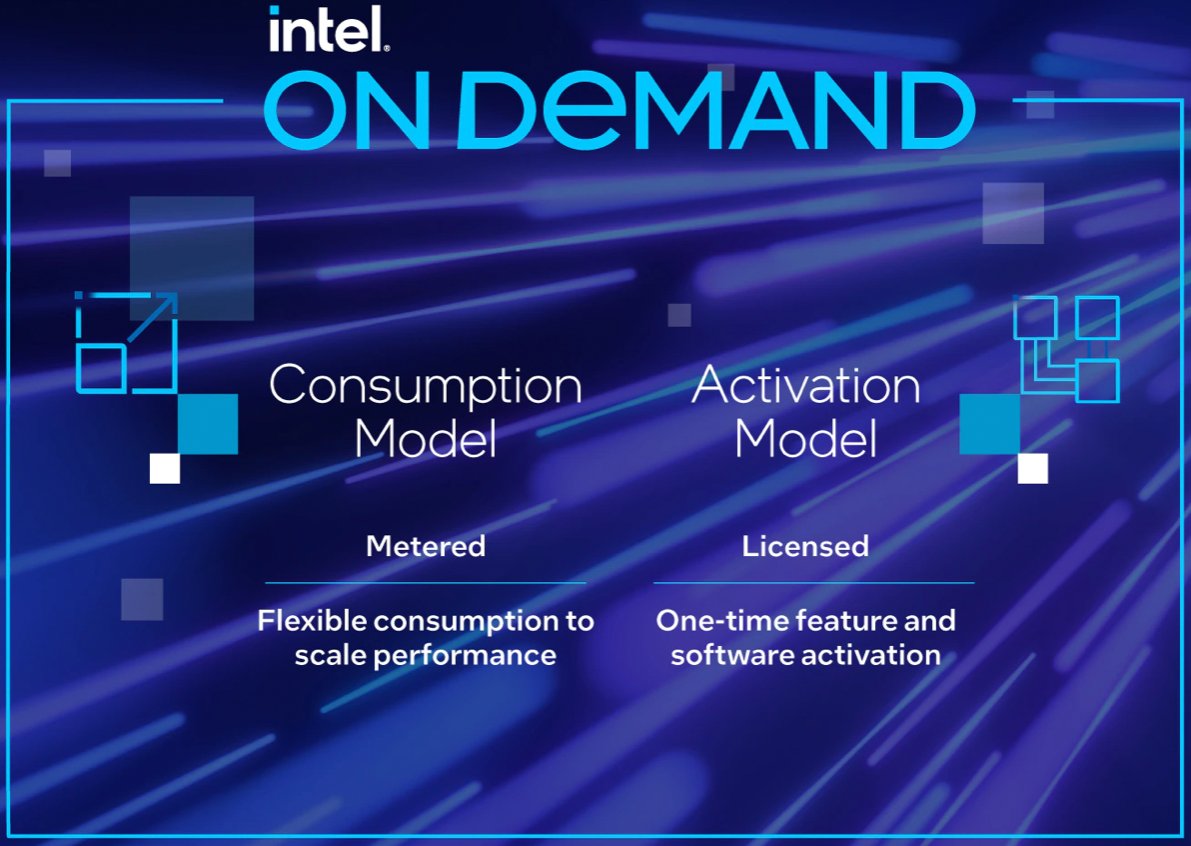

Technical Mechanics and Accelerator Economics

The SDSi framework—marketed as Intel On Demand—targeted 4th Generation Xeon Scalable processors (codenamed Sapphire Rapids) fabricated on Intel 7 process nodes. It allowed enterprises to activate physically embedded accelerators via license keys post-purchase. Key hardware blocks included:

- Dynamic Load Balancer (DLB): Packet processing workload optimization

- Data Streaming Accelerator (DSA): 20% faster data movement for storage/networking

- In-Memory Analytics Accelerator (IAA): Up to 2.8x database query throughput

- QuickAssist Technology (QAT): 100Gbps encryption/compression offload

The model offered two payment structures: permanent unlocks ($350-$2,000 per socket) or usage-based billing. Benchmarks showed activated accelerators improving specific workloads by 15-40% compared to base configurations. However, SDSi required dedicated motherboard infrastructure for license validation, adding $15-$30 per unit in BOM costs.

Market Rejection and Supply Chain Fallout

SDSi faced immediate backlash from OEMs and hyperscalers, who criticized Intel for "double-dipping" on silicon already manufactured and shipped. Industry analysis revealed three core failures:

- Economic Flaws: Enterprises rejected paying premiums for hardware physically present in chips they already purchased. Server vendors reported <5% adoption rates in 2023-2024.

- Supply Chain Complexity: The licensing mechanism introduced firmware validation hurdles that delayed server deployments by 3-5 weeks, conflicting with just-in-time manufacturing principles.

- Competitive Pressure: AMD’s EPYC processors offered comparable accelerators without activation fees, capturing 30.7% of the server market by Q4 2024—a 12-point gain since SDSi’s launch.

Intel’s discontinuation aligns with its Xeon 6 roadmap, which consolidates accelerators into default configurations. The company’s recent foundry struggles—including Intel 4 node yield issues delaying Sierra Forest chips—likely accelerated SDSi’s demise as resources shifted to core production challenges.

Strategic Implications

The SDSi failure underscores a critical lesson in semiconductor monetization: hardware-based software licensing faces existential resistance in enterprise markets. Analyst projections indicate Intel will absorb a $120M R&D write-down but avoid long-term brand damage by removing the program before Granite Rapids launches. Competitors like Ampere Computing now dominate the "as-a-service" silicon model with cloud-native designs, while Intel refocuses on process leadership and open-source acceleration frameworks like oneAPI.

For server buyers, SDSi’s termination eliminates licensing overhead but removes workload-specific optimization flexibility. Future performance gains will require socket upgrades rather than software unlocks—a trade-off favoring simplicity over granular control as Intel prioritizes yield recovery and market share defense.

Comments

Please log in or register to join the discussion