Microsoft introduces Fabric IQ, a revolutionary platform that breaks down regulatory silos by creating unified ontologies across financial sectors, enabling proactive supervision of interconnected risks in digital financial ecosystems.

The financial regulatory landscape is undergoing a fundamental transformation as digital financial services create increasingly complex risk ecosystems. Traditional regulatory approaches that analyze banking, capital markets, and P2P lending in isolation are no longer adequate when a struggling P2P platform can trigger cascading effects across multiple sectors. Microsoft has addressed this challenge with Fabric IQ, a comprehensive platform that combines data lakehouse capabilities, semantic modeling, ontology generation, and planning tools to create a unified view of financial risk.

The Evolution of Financial Regulation

Financial regulators worldwide have struggled to keep pace with the rapid growth of digital financial services. Peer-to-peer lending platforms, digital banks, and insurtech providers have created an environment where risks transcend traditional regulatory boundaries. A single P2P lending platform's distress can affect the banks that fund it, the insurers that underwrite its credit risk, and ultimately the consumers who borrow through it.

Indonesia's financial regulator has been at the forefront of addressing this complexity, having automated parts of its supervisory analysis. However, like most regulatory frameworks, it still operates largely in silos, with banking data analyzed separately from capital market data, and P2P lending statistics treated independently from insurance metrics.

Microsoft Fabric IQ introduces a fundamentally new approach to solving this problem by creating a unified ontology that connects previously disparate data sources and regulatory domains. The platform provides two powerful components working in tandem: a semantic data model that defines analytical relationships, and an ontology layer that transforms these relationships into machine-understandable business entities governed by regulatory rules.

Architectural Innovation: From Siloed Data to Unified Ontology

The Fabric IQ architecture represents a significant departure from traditional data warehousing approaches for financial regulation. Instead of creating separate data marts for each regulatory domain, the platform establishes a unified foundation through three core components:

First, a Lakehouse ingests publicly available data including bank financials, P2P lending statistics, borrower demographics, and licensing information. This serves as the bronze and silver layer of a medallion architecture, storing both raw ingested data and transformed analytical tables in a governed, queryable format.

Second, a Semantic Model organizes these tables into a star schema with proper relationships, hierarchies, and measures. This Power BI construct serves as the analytical interface and later becomes the blueprint for generating the ontology.

Third, and most significantly, an Ontology elevates these tables into business entities such as Bank, P2P Platform, Borrower, and Loan, connected by meaningful relationships and governed by regulatory rules. This is where Fabric IQ truly differentiates itself from traditional BI solutions, creating a machine-understandable vocabulary of the financial ecosystem.

Implementation: Building a Cross-Sector Regulatory Solution

Implementing a Fabric IQ solution for financial regulation involves four key steps that transform raw data into actionable regulatory intelligence.

Step 1: Data Foundation in Fabric Lakehouse

Every Fabric IQ solution begins with a well-structured Lakehouse that holds source data in a governed and queryable format. For the Indonesian regulatory use case, the Lakehouse contains dimension tables for bank profiles, borrower demographics, P2P lending operators, individual loans, and supervisory teams, plus relationship tables that capture connections between entities.

This dimensional modeling approach ensures clear separation between entities and their relationships, enabling the subsequent semantic and ontology layers to function effectively. The Direct Lake mode ensures that when regulators publish updated monthly statistics, the entire system reflects the latest data without requiring manual intervention.

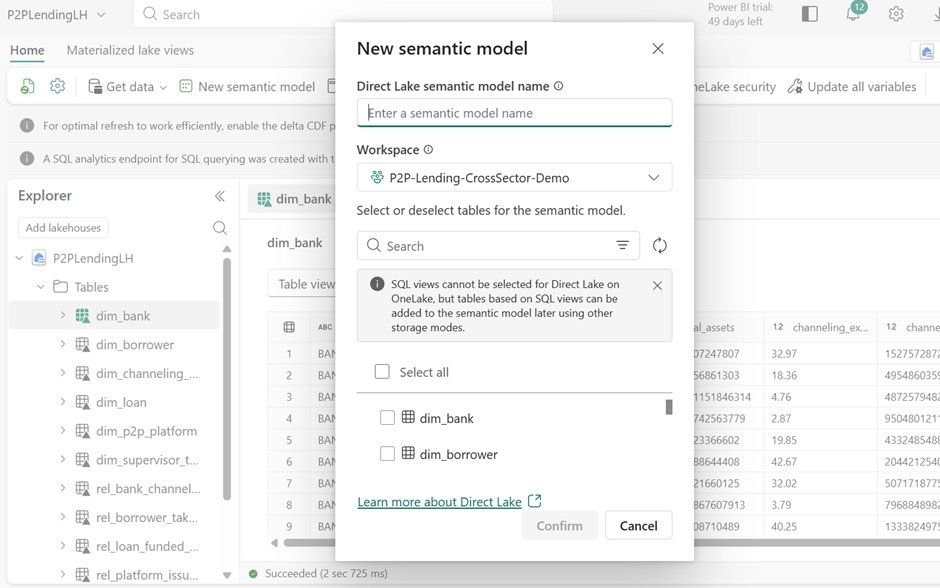

Step 2: Creating the Semantic Model

With data established in the Lakehouse, the next step is creating a Semantic Model that defines the analytical interface. This Power BI construct organizes tables into a star schema with proper relationships, hierarchies, and measures. Critically, the Semantic Model serves as the blueprint from which the Ontology is generated.

The model configuration process involves verifying that all necessary relationships are correctly established—such as connecting banks to the P2P platforms they fund, and linking borrowers to their loans. At this stage, regulators can also add calculated measures, such as weighted average TWP90 (Time Within 90 Days) across platforms funded by a specific bank, or total channeling exposure as a percentage of a bank's assets.

Step 3: Generating the Ontology

This is where Fabric IQ's innovation truly shines. The Ontology transforms the Semantic Model from a reporting layer into an intelligence layer. While the Semantic Model answers "what does the data look like," the Ontology answers "what does the data mean" by creating a machine-understandable vocabulary of the financial ecosystem.

The Ontology consists of entity types (Bank, Borrower, P2P Platform), properties (NPL ratio, TWP90 rate), and relationships (Bank channels funding to P2P Platform). Beyond static modeling, it supports rules and constraints that trigger automated actions when business conditions are met.

For the Indonesian regulatory use case, the Ontology incorporates rules such as:

- Flagging P2P platforms with TWP90 exceeding 5% as high risk

- Alerting banking supervisors when channeling exposure to flagged platforms exceeds 10% of portfolio

- Triggering consumer protection reviews when young borrowers are overleveraged

- Escalating to senior supervisors when bank CAR drops below 10% with active P2P channeling

These rules integrate with Fabric Activator, enabling automatic initiation of business processes through alerts and automated actions when regulatory thresholds are crossed.

Step 4: Setting Up Planning Sheets

While the Ontology identifies current risks, the Planning component helps supervisors decide what should happen next. Planning brings budgeting, forecasting, and scenario modeling directly into the same environment where data lives, eliminating the disconnect between analytical insights and forward-looking decisions.

Planning sheets can incorporate risk metrics alongside budget dimensions, enabling supervisors to prioritize examinations based on risk categories. For example, with multiple platforms showing "Very High" risk, supervisors can forecast warning letter volumes, allocate examination budgets, and model scenarios based on live data.

Competitive Landscape and Strategic Positioning

Microsoft Fabric IQ enters a market where traditional regulatory technology solutions have struggled to address the interconnected nature of modern financial risks. Unlike conventional BI platforms that focus primarily on reporting and visualization, Fabric IQ emphasizes semantic understanding and automated reasoning.

In comparison to specialized regulatory technology providers, Fabric IQ offers several advantages:

- Integration with Microsoft's broader cloud ecosystem, including Azure and Power Platform

- Unified approach that avoids the need for multiple specialized tools

- Advanced AI capabilities through the Ontology layer

- Built-in planning and budgeting functionality

However, Fabric IQ faces competition from both established enterprise vendors with regulatory solutions and emerging AI-powered governance platforms. Its success will depend on demonstrating clear ROI for regulators through reduced risk, more efficient resource allocation, and proactive identification of systemic threats.

Business Impact and Future Outlook

The implementation of Fabric IQ for financial regulation represents a paradigm shift from reactive to proactive supervision. By creating a unified ontology of the financial ecosystem, regulators can identify and address risks before they escalate into crises.

For financial institutions, this approach means more sophisticated supervision that can detect patterns across business lines and regulatory domains. While this may increase compliance complexity, it also provides clearer visibility into how their activities fit into the broader financial ecosystem.

As digital financial services continue to evolve, solutions like Fabric IQ will become essential for maintaining financial stability. The platform's ability to incorporate new data sources, update regulatory rules, and model emerging risks positions it as a strategic tool for regulators navigating the increasingly complex financial landscape.

Microsoft's Fabric IQ exemplifies the convergence of cloud technology, AI, and domain expertise to solve complex regulatory challenges. By breaking down silos and creating a unified understanding of financial risk, it offers a blueprint for how regulatory technology must evolve to address the realities of modern finance.

Comments

Please log in or register to join the discussion