Build‑to‑Rent (BTR) has grown from a niche response to the 2008 crisis into a multi‑billion‑dollar segment of U.S. housing, now accounting for over 7 % of new single‑family starts. Its rapid expansion, the policy backlash embodied in the Senate’s 21st Century ROAD to Housing Act, and the mixed evidence on how institutional rental owners affect prices and rents make BTR a pivotal, if contested, piece of the affordability puzzle.

The Rise of Build‑to‑Rent Housing

By Brian Potter – May 21 2026

A New Chapter in the Housing Story

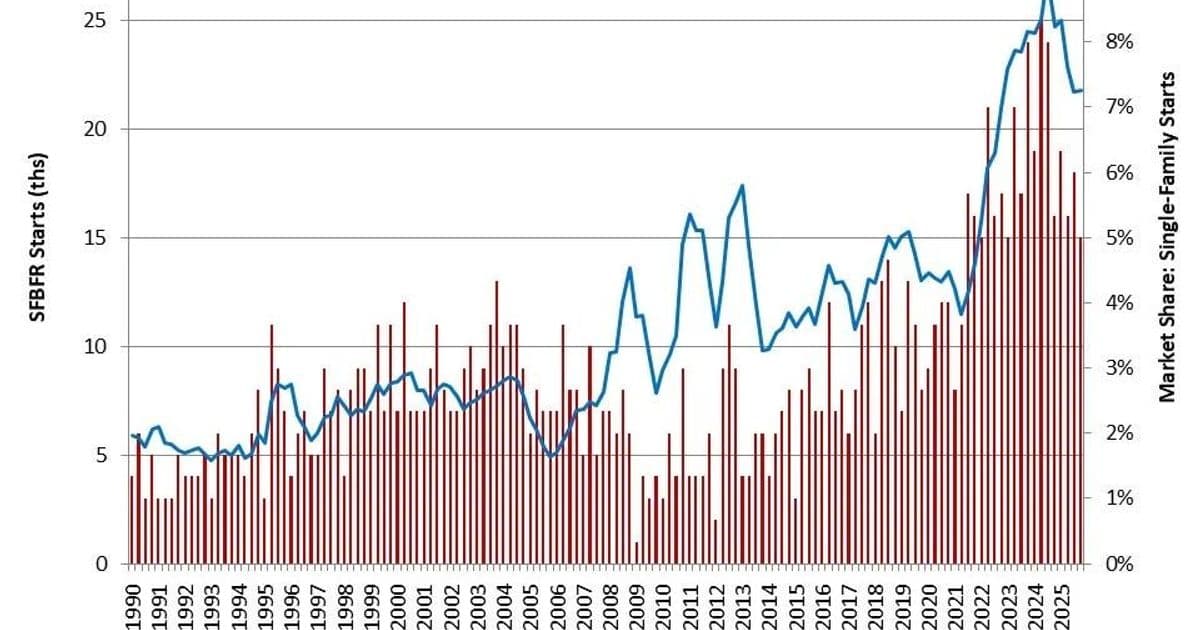

The United States is witnessing a transformation that would have seemed improbable a generation ago: developers are constructing entire neighborhoods of single‑family homes specifically to rent them out. According to the National Association of Homebuilders, BTR homes have climbed from less than 2 % of new starts in the 1990s to more than 7 % today. In 2025 alone, at least 68 000 such homes broke ground, and the true figure may be well above 100 000 once data gaps are accounted for.

The sector’s momentum has collided with federal policy. The Senate’s 21st Century ROAD to Housing Act contains Section 901, which would force any institutional investor that owns more than 350 single‑family rentals to sell its BTR portfolio to individual homeowners after seven years. Because the BTR model hinges on the owner retaining the property to generate rental cash flow, the provision threatens the core economics of the industry. Since the bill’s announcement, financing for new BTR projects has all but stalled as investors wait for legislative clarity.

Over a hundred pro‑housing organizations—ranging from the Berkeley Terner Center to the NAHB—have rallied against the provision, warning that it could shrink short‑term housing supply at a moment when demand is surging.

Origins: From Foreclosure Fallout to Institutional Rental Empires

The modern BTR landscape is a direct outgrowth of the 2008 Global Financial Crisis. Before the crisis, single‑family rentals existed but were dominated by small, scattered landlords. By 2011, no single company owned more than 1 000 rental homes. The crisis, however, produced two forces that reshaped the market:

- Massive foreclosures – four million homes entered the market between 2007 and 2010, driving home values down 26 % nationally and as much as 60 % in places like Las Vegas.

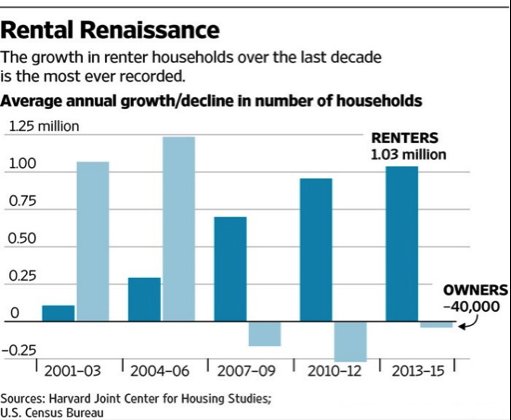

- Tightened credit – mortgage qualification scores rose by over 50 points, pushing the home‑ownership rate from 69 % in 2005 to 63 % in 2016.

These dynamics pushed millions of households into renting while flooding the market with cheap, distressed properties. Investment firms seized the opportunity. Treehouse Group bought 11 000 Phoenix homes in 2010; after Blackstone’s 2012 acquisition, it became Invitation Homes, now with over 86 000 rentals. Parallel ventures—American Homes 4 Rent, Tricon, and others—followed the same playbook, rapidly scaling to control more than 200 000 homes by 2022.

Government programs also nudged the market in this direction. The REO‑to‑Rental Initiative (2012) allowed pre‑qualified investors to bid on foreclosed portfolios, and Fannie Mae’s 2017 billion‑dollar loan to Invitation Homes further legitimized institutional rental ownership.

From Buying to Building: The Birth of BTR

While early investors focused on acquiring and refurbishing existing homes, a handful of companies began building homes expressly for rent. Notable pioneers include:

- NexMetro (Phoenix, 2012) – first community completed in 2015; now over 10 000 BTR homes under the Avilla Homes brand.

- BB Living (Phoenix, 2012) – operates 18 BTR communities.

- AHV Communities (Texas, 2014) – launched a dozen projects over twelve years.

Building from the ground up offered clear advantages: lower maintenance costs, designs optimized for durability, and the ability to cluster homes for operational efficiency. As the pool of cheap existing homes dried up, the largest rental firms—American Homes 4 Rent, Invitation Homes, Pretium Partners—pivoted to BTR as their primary acquisition strategy.

Homebuilders also entered the fray. Lennar launched Quarterra (2020), DR Horton began BTR construction in 2019 and sold nearly 3 500 BTR homes last year, and Taylor Morrison introduced the Yardly brand in 2022. For builders, BTR provides a steady pipeline of work and a hedge against uncertain sales to individual buyers.

What Do BTR Homes Look Like?

BTR is not a monolith; it spans a spectrum from detached single‑family houses to horizontal multifamily clusters that feel more like low‑rise apartments. The three main sub‑categories are:

- Detached single‑family – homes indistinguishable from buyer‑owned houses, each on its own parcel with a garage and yard. Tricon’s Palomino Ranch in Houston exemplifies this model.

- Single‑family attached – townhomes or duplexes sharing walls, offering a blend of privacy and density. BB Living’s Val Vista in Gilbert, Arizona, illustrates this approach.

- Horizontal multifamily – spread‑out apartment‑style complexes with 1‑ to 3‑bedroom units, shared amenities, and often no garages. NexMetro’s Avilla Homes Deer Valley in Phoenix falls into this category.

Across all types, developers design for low operating costs: durable interior finishes, standardized unit layouts, and aggressive property‑tax appeal programs. American Homes 4 Rent reports that its maintenance expenses are only 25 % of those for its purchased‑home portfolio, and its tax‑appeal team files more than 25 000 appeals annually.

Where Is BTR Growing?

The Sun Belt dominates BTR construction. Texas, Florida, and Arizona together host about 60 % of all new BTR units, with Georgia and North Carolina rounding out the top five. Within those states, activity clusters around major metros—Phoenix, Dallas/Houston, Atlanta—where population growth, land availability, and relatively permissive zoning policies align.

Why Do Renters Choose BTR?

Two intertwined forces drive demand:

- Affordability pressures – Since 2012, home prices have outpaced inflation and median income. Post‑COVID interest‑rate spikes made mortgage payments steep, pushing many households toward renting larger spaces.

- Lifestyle preferences – A growing segment of renters—retirees, remote workers, and those simply avoiding the responsibilities of ownership—value the flexibility and lower upkeep that BTR offers.

Surveys from the Amherst Group (2021) and NexMetro (2024) show that a majority of renters would not qualify for a mortgage due to credit or income constraints, yet still desire the space and neighborhood quality that single‑family homes provide.

BTR’s Impact on Prices and Rents: A Mixed Evidence Base

The broader debate over institutional ownership of single‑family rentals is contentious. Studies such as Mills et al. (2015) and Lambie‑Hanson et al. (2019) suggest that large investors can support house‑price appreciation, especially in markets where they own a sizable share of the rental stock. Conversely, Hanson (2024) argues that price gains often reflect underlying market fundamentals rather than investor activity.

When it comes to rents, the picture is similarly nuanced. Some research (Lee & Wylie 2024; Gurun et al. 2023) finds that institutional landlords raise rents above market averages, leveraging scale and data‑driven pricing. Other analyses (Coven 2025; Wang & Zhai 2026) highlight the supply‑side effect of adding thousands of new rental units, which can moderate rent growth.

Importantly, most of this literature examines buy‑to‑rent—the purchase of existing homes—not build‑to‑rent. BTR creates new housing supply, which could offset any upward pressure on rents, but it might also reduce the stock of homes built for sale, potentially nudging purchase prices higher. Because rigorous empirical work on BTR is still scarce, policymakers are navigating a debate with limited data.

Policy Implications and Counter‑Perspectives

The Senate’s Section 901 provision reflects a protective impulse: preventing large investors from monopolizing the rental market and preserving home‑ownership opportunities. Critics argue that the measure is overly blunt, penalizing a business model that expands the overall housing stock and offers renters a quality‑controlled product.

Supporters of the provision contend that institutional concentration—in some metros, up to 25 % of rentals—can distort local markets, limit home‑ownership pathways, and give corporations undue political influence.

A more nuanced approach might involve:

- Targeted zoning reforms that lower construction costs and speed up permitting for both for‑sale and rental projects.

- Incentives for affordable‑unit inclusion within BTR communities, akin to inclusionary‑housing policies for condos.

- Data‑driven caps that trigger only when institutional ownership exceeds a market‑specific threshold, rather than a blanket 350‑home rule.

Looking Ahead: What Must Happen?

The fundamental driver behind BTR’s rise is housing unaffordability. Whether a household buys or rents, the scarcity of affordable space forces difficult trade‑offs. Shutting down BTR would remove a significant source of new, professionally managed rental housing, potentially worsening the shortage.

The longer‑term solution lies in expanding the overall housing supply and reducing construction costs—through modular building, streamlined approvals, and innovative financing. If the market can produce more homes at lower prices, the pressure that fuels both high purchase prices and high rents will ease, and the political appetite for punitive restrictions on rental investors will wane.

Conclusion

Build‑to‑Rent has evolved from a crisis‑driven workaround into a legitimate, growing segment of the U.S. housing ecosystem. It offers renters larger, well‑maintained homes and gives developers a steady pipeline of work. While concerns about institutional concentration are not unfounded, the evidence suggests that the net effect of BTR—when it adds genuine new supply—tends to benefit consumers by expanding choice and moderating rents.

Policymakers should therefore focus on removing barriers to construction, encouraging affordable‑unit integration, and gathering better data on BTR’s market impact rather than imposing sweeping bans that could choke a nascent source of much‑needed housing.

For further reading, see the NAHB’s housing‑start data, the Federal Housing Finance Agency’s REO‑to‑Rental pilot report, and the latest investor presentations from Invitation Homes, American Homes 4 Rent, and NexMetro.

Comments

Please log in or register to join the discussion