Q1 2026 market data reveals AMD's continued growth in server and mobile segments while Intel retains consumer PC leadership, with both companies competing fiercely across different market segments.

The first quarter of 2026 marked a significant turning point in the x86 CPU landscape, with AMD achieving record-breaking revenue shares in server segments while maintaining strong growth in mobile processors, despite Intel's continued dominance in the consumer PC market. According to data from Mercury Research, AMD's strategic focus on high-performance, high-margin processors has enabled the company to capture substantial market value even as Intel maintains shipment leadership.

Market Share Breakdown: A Tale of Two Segments

AMD's overall x86 CPU revenue share reached 38.1% in Q1 2026, reflecting the company's successful strategy of targeting premium segments across different market categories. The most dramatic shift occurred in the server space, where AMD's EPYC processors captured 46.2% of x86 server CPU revenue while shipping 33.2% of units. This significant gap between unit share and revenue share indicates AMD's success in commanding higher average selling prices (ASPs) through its high-core-count configurations and competitive performance-per-watt metrics.

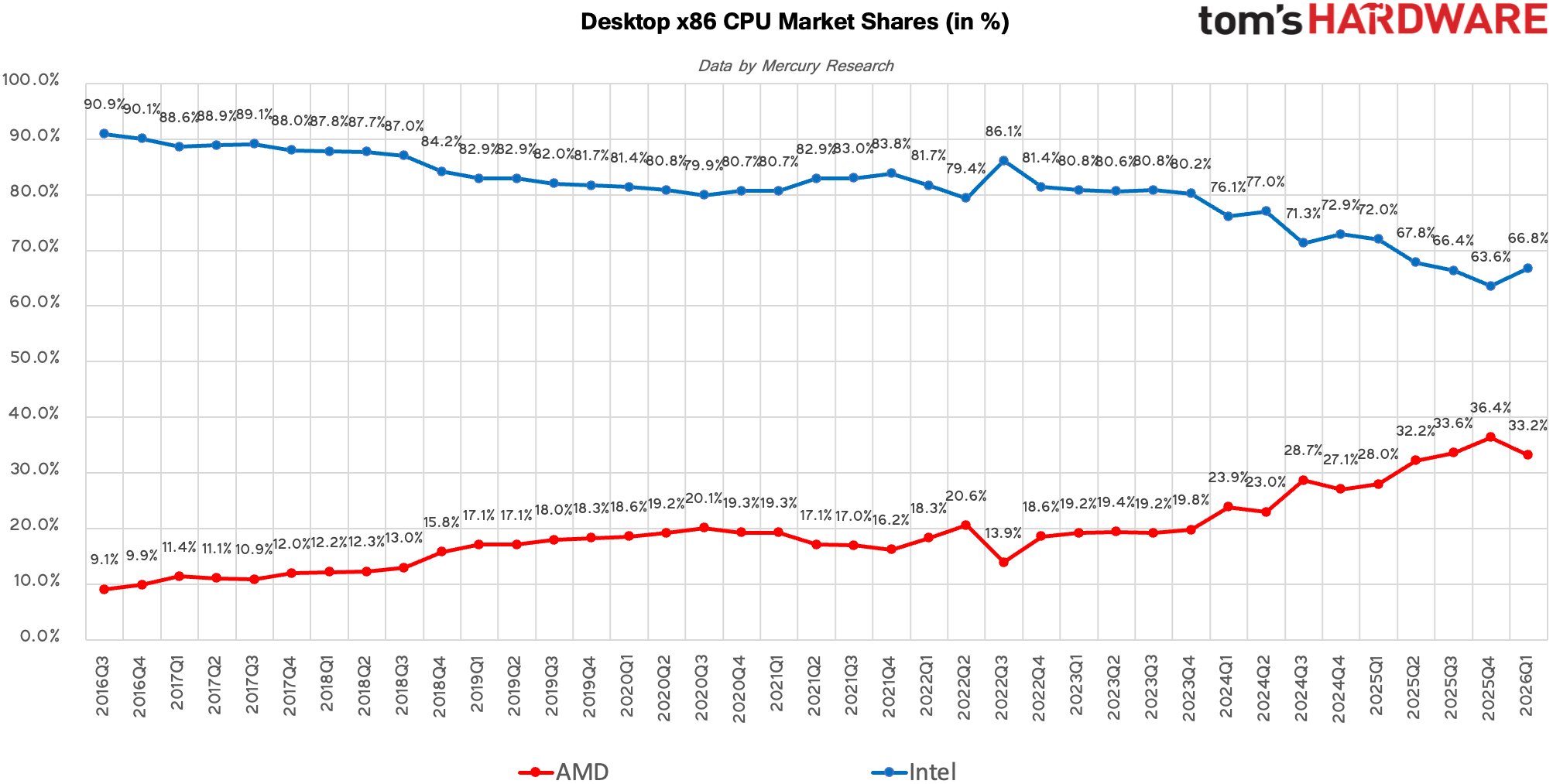

In the consumer PC segment, AMD's client CPU unit share rose to 29.6%, up from 29.2% in Q4 2025 and significantly higher than the 24.1% recorded in Q1 2025. However, Intel maintained a commanding 70.4% share of the consumer PC market, though this represents a decline from its 75.9% share in Q1 2025, suggesting AMD's gradual but steady encroachment on Intel's traditional stronghold.

Desktop vs. Mobile: Diverging Trajectories

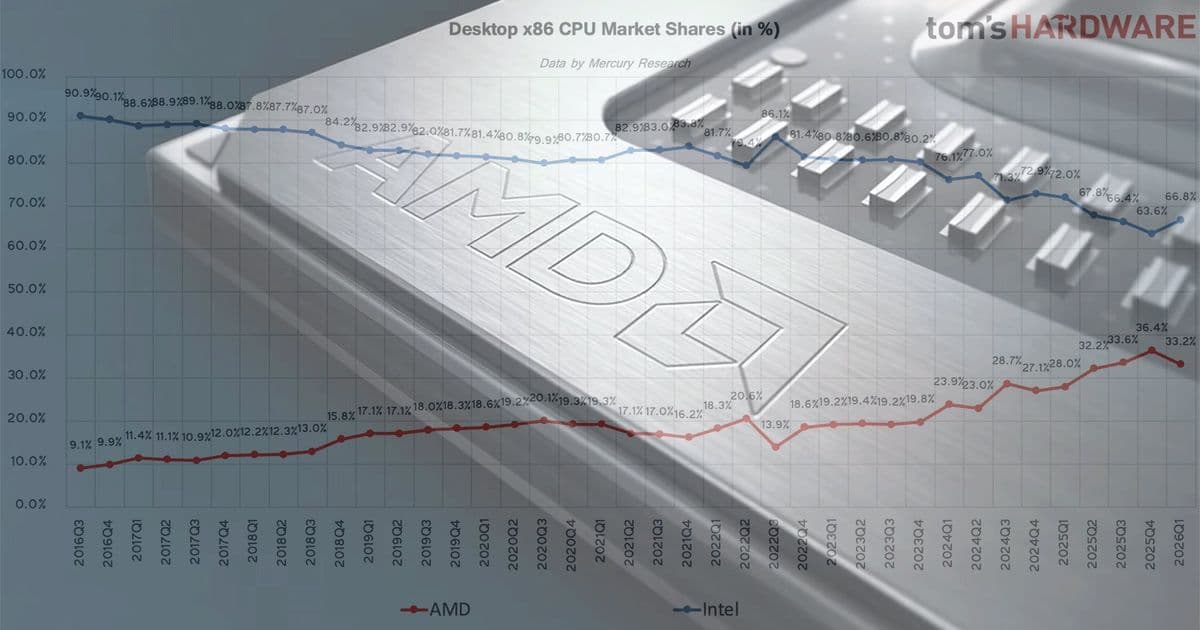

The quarter revealed contrasting performance between desktop and mobile segments for AMD. In desktops, the company's unit share declined sequentially to 33.2% from a record 36.4% in Q4 2025, though it remained well above the 28% recorded in Q1 2025. Intel regained some ground in desktops, increasing its share to 66.8%, but remained below its year-ago level of 72%. Despite the sequential dip, AMD maintained a strong 37.6% revenue share in desktops, indicating continued success with its premium Ryzen processors.

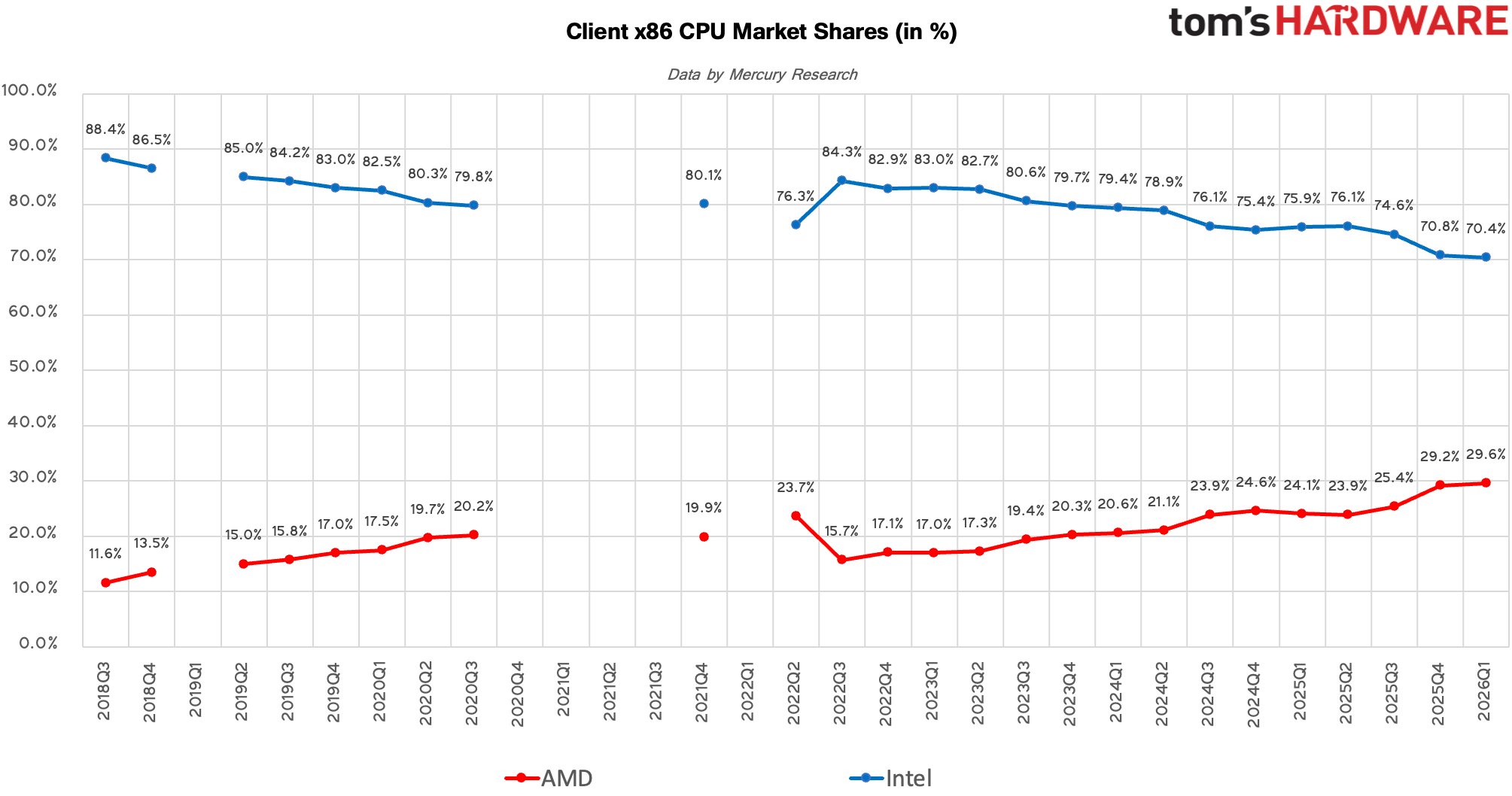

The mobile segment told a different story, with AMD achieving its best-ever performance in notebooks. The company's mobile CPU unit share climbed to 28.3%, up from 26% in Q4 2025 and 22.5% in Q1 2025. This growth reflects AMD's improved product availability and expanded footprint in business and commercial notebooks, segments traditionally dominated by Intel. On the revenue side, AMD's mobile CPU revenue share rose to 28.9%, up from 24.9% in Q4 2025 and 22.2% in Q1 2025, demonstrating increasing competitiveness in higher-margin premium laptops.

Server Market Transformation: AMD's Strategic Breakthrough

The server segment represented AMD's most significant achievement in Q1 2026, with the company's EPYC processors achieving a 33.2% unit share, up from 28.8% in Q4 2025 and 27.2% in Q1 2025. More impressively, AMD's server revenue share jumped to 46.2%, a 5% increase in a single quarter, meaning the company now commands nearly half of all x86 server CPU revenue.

This remarkable performance stems from several factors:

- AMD's continued leadership in performance-per-watt metrics, particularly important for hyperscale data centers

- Strong adoption among cloud providers and AI/HPC infrastructure operators

- Competitive pricing strategies for high-core-count configurations

- Successful execution of their 3D V-Cache technology in server applications

Intel, while still shipping 66.8% of server processors, has seen its position weaken both sequentially and year-over-year. The gap between Intel's unit share and AMD's revenue share highlights the differing ASPs between Xeon and EPYC processors, with AMD commanding premium prices for their high-performance configurations.

Technical Context and Competitive Positioning

AMD's success can be attributed to several technical advantages:

Process Technology: AMD's use of TSMC's advanced 5nm and 4nm processes for their latest EPYC and Ryzen processors has provided a competitive edge over Intel's 10nm and 7nm implementations.

Chiplet Architecture: AMD's chiplet-based design approach has enabled better yields, lower costs, and more flexible product segmentation compared to Intel's monolithic designs.

Memory Performance: AMD's continued leadership in memory bandwidth and latency has been particularly advantageous in server and high-performance computing applications.

Power Efficiency: The performance-per-watt advantage has become increasingly critical as data centers face pressure to reduce energy consumption and cooling costs.

Market Implications and Future Outlook

The market share data reveals several important trends:

Premium Segment Focus: AMD's ability to capture significant revenue share despite lower unit shares indicates success in targeting higher-margin segments, particularly in servers and premium notebooks.

Intel's Response Strategy: Intel's upcoming Nova Lake processors for client systems represent the company's attempt to regain momentum in the consumer space. The success of these processors will be critical to Intel's competitive position in the second half of 2026.

Server Market Dynamics: AMD's continued growth in servers suggests that the company has established itself as a credible alternative to Intel in enterprise and cloud environments, a significant shift from just a few years ago.

Manufacturing Considerations: Both companies face challenges in their manufacturing roadmaps, with Intel's transition to new process technologies and AMD's reliance on TSMC capacity potentially creating supply constraints or competitive advantages depending on execution.

Looking ahead, the competitive landscape will likely intensify as Intel launches its next-generation processors and AMD continues to refine its product portfolio. The server segment, in particular, represents a high-stakes battleground where both companies are investing heavily in R&D to gain competitive advantages in performance, efficiency, and specialized workloads like AI and HPC.

For AMD, the challenge will be maintaining momentum across multiple segments while managing supply chain constraints and potential competitive responses from Intel. For Intel, the focus will be on regaining ground in consumer PCs while defending its enterprise server dominance through upcoming product launches and manufacturing improvements.

The data from Q1 2026 suggests that the x86 CPU market is entering a period of intensified competition, with both companies finding success in different segments. AMD's growing revenue shares indicate its ability to compete effectively in premium markets, while Intel's continued shipment leadership demonstrates its broad market presence and channel strength. The coming quarters will likely see this competitive dynamic continue to evolve as both companies execute on their product roadmaps and respond to each other's moves.

Comments

Please log in or register to join the discussion