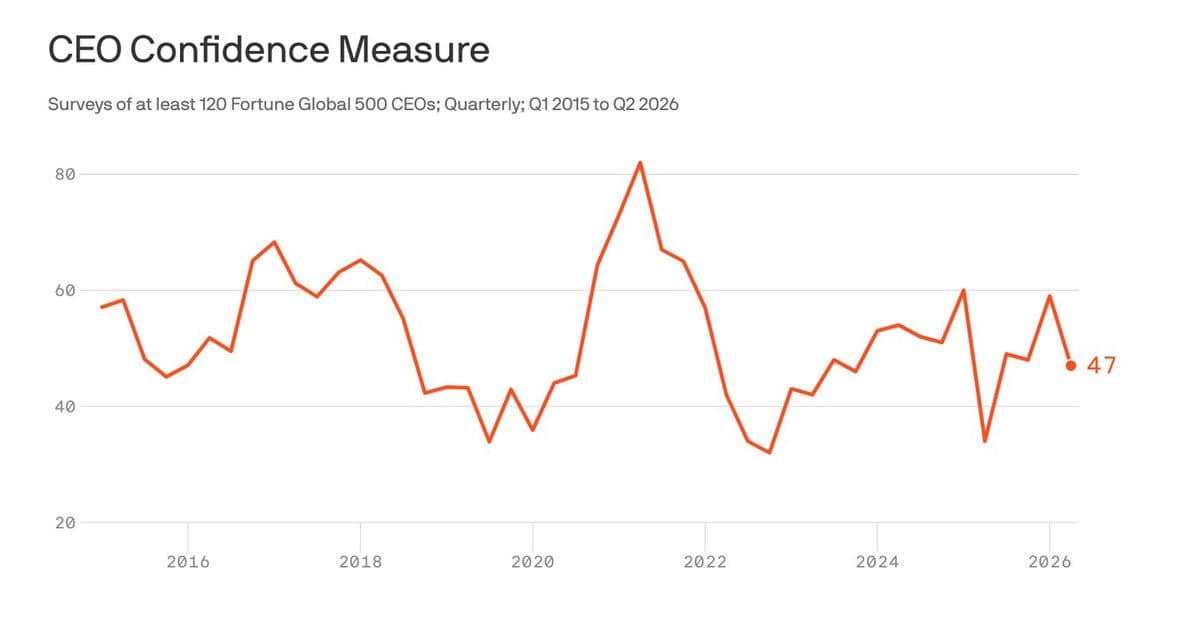

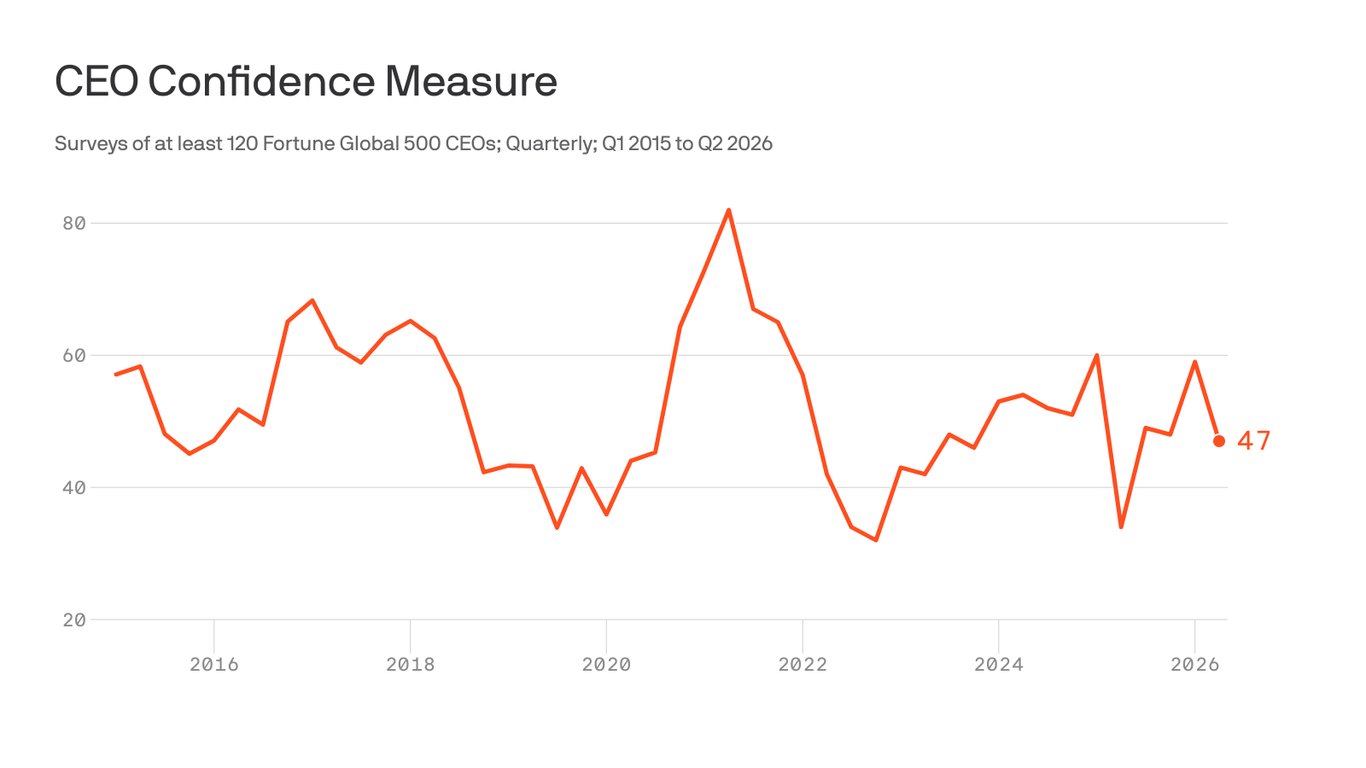

A new Axios‑Harris poll of 1,200 public‑company CEOs reveals confidence in the U.S. economy fell to 32 %, the weakest level since 2019, driven by tighter credit, slower consumer spending and lingering supply‑chain disruptions.

CEO Confidence Slumps to 5‑Year Low, Survey Shows

A fresh Axios‑Harris survey released on May 27 2026 shows U.S. chief executive officers are markedly less optimistic about the near‑term economy. Only 32 % of the 1,200 CEOs surveyed said they expect growth in the next 12 months, down from 44 % a year earlier and the lowest reading since the pre‑pandemic survey in 2019.

Market context

| Metric (Q1 2026) | Q4 2025 | YoY change |

|---|---|---|

| CEO confidence index | 32 % | –12 pp |

| Corporate borrowing cost (average 10‑yr LIBOR‑plus) | 5.8 % | +0.6 pp |

| Consumer confidence (University of Michigan) | 68.2 | –4.5 pp |

| Manufacturing PMI (ISM) | 48.7 | –2.3 pp |

| S&P 500 total return | 4.1 % | –1.2 pp |

The data line up with several macro‑level pressures:

- Credit tightening – The Federal Reserve’s policy rate sits at 5.25‑5.50 %, the highest in 22 years. Banks have tightened underwriting standards, pushing average corporate borrowing costs above 5 % for the first time since 2018.

- Consumer slowdown – Retail sales grew 1.2 % YoY in Q1, well below the 3.4 % expansion in Q4 2025. Disposable‑income growth has stalled as wages lag behind inflation, now at 2.8 % versus 3.6 % price growth.

- Supply‑chain friction – The Bloomberg Global Shipping Index remains 18 % above pre‑pandemic levels, keeping inventory‑holding costs high for manufacturers.

- Geopolitical risk – Ongoing tensions in the Indo‑Pacific have forced many firms to reconsider offshore production, adding to capital‑expenditure uncertainty.

These forces collectively erode the confidence that CEOs traditionally draw from stable financing conditions and robust consumer demand.

What it means for investors and strategy

- Capital‑allocation slowdown – Companies are likely to defer or scale back cap‑ex projects. In the last quarter, announced capital spending fell to $1.4 trillion, a 9 % drop from the previous quarter. Sectors that rely heavily on long‑lead‑time investments, such as semiconductor fabs and renewable‑energy parks, may see delayed roll‑outs.

- M&A activity could wane – Deal volume in Q1 2026 slipped to $210 billion, the lowest since 2020. Private‑equity firms are reporting tighter fundraising cycles, suggesting a broader pull‑back in leveraged transactions.

- Dividend policy pressure – With earnings forecasts trimmed by an average of 5 % across the S&P 500, boards may prioritize cash preservation over dividend hikes. Investors should monitor payout ratios, especially in consumer‑discretionary and industrials.

- Risk‑adjusted valuation shifts – The S&P 500 price‑to‑earnings multiple fell to 22.1x, down from 24.3x a year ago. Discounted‑cash‑flow models that previously used a 7 % discount rate now incorporate a higher risk premium, pushing target prices lower for many growth stocks.

- Strategic pivots to resilience – Firms are increasing spend on supply‑chain visibility tools and on‑shoring initiatives. According to a Deloitte 2026 supply‑chain survey, 38 % of CEOs plan to relocate at least 15 % of production capacity back to North America within the next 24 months.

Outlook

While the confidence dip is pronounced, it is not unprecedented. The index fell similarly during the 2015‑16 oil‑price shock, after which a gradual recovery in credit conditions helped restore optimism. Analysts will watch the Federal Reserve’s policy stance closely; any signal of rate easing could provide a modest boost to CEO sentiment.

For investors, the key takeaway is to re‑evaluate exposure to sectors that are most sensitive to financing costs and consumer demand. Companies that have already diversified their supply chains and maintain strong balance sheets are likely to weather the current headwinds better than those still heavily leveraged.

Data sources: Axios‑Harris CEO Survey, Federal Reserve Economic Data (FRED), Bloomberg Shipping Index, Deloitte Supply‑Chain Survey, S&P 500 quarterly reports.

Comments

Please log in or register to join the discussion