American households are increasingly spending beyond their earnings, creating a financial squeeze that could impact economic growth and consumer behavior in the coming months.

American consumers are spending money faster than they earn it, a trend that could reshape economic dynamics in the coming months. According to the latest data from the Bureau of Economic Analysis, personal consumption expenditures grew by 0.8% in April, while personal income increased by just 0.4%. This widening gap between spending and earnings signals growing financial pressure on U.S. households.

The spending surge comes amid persistent inflation, which has eroded purchasing power despite recent cooling. Consumer prices rose 3.4% year-over-year in April, remaining above the Federal Reserve's 2% target. This combination of rising prices and stagnant wage growth has forced many households to draw down savings and increase borrowing to maintain their standard of living.

"We're seeing a concerning pattern where consumers are dipping into savings and taking on more debt to keep up with expenses," said Sarah Johnson, senior economist at the Federal Reserve Bank of New York. "While this can support short-term economic activity, it's not sustainable over the long term."

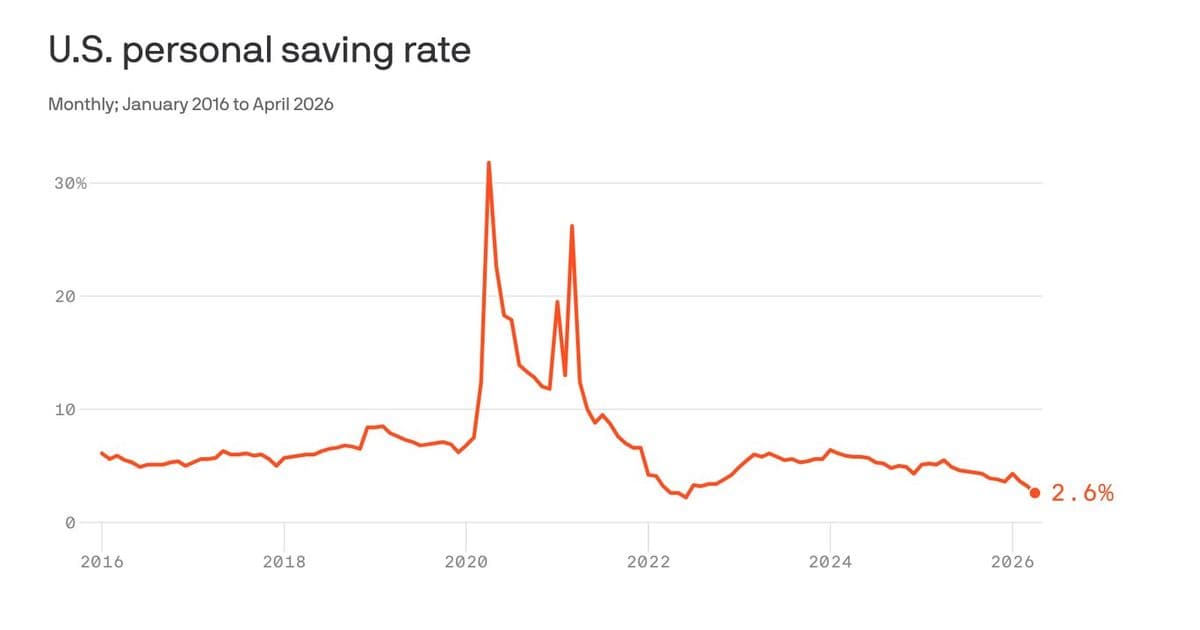

Savings rates have fallen significantly from pandemic highs. The personal savings rate stood at 4.1% in April, down from 33.8% in April 2020, according to the Bureau of Economic Analysis. Credit card debt has reached record levels, with total revolving credit climbing to $1.21 trillion in the first quarter of 2023, according to the Federal Reserve.

The spending patterns vary across income groups. Higher-income households continue to spend on services like travel and dining, while lower-income households focus on necessities. This divergence is reflected in retail sales data, which show strong performance in sectors like restaurants and travel agencies, but more modest gains in discount retail.

Retail sales data from the Census Bureau reveals that spending on services has outpaced goods for several consecutive months. In April, sales at food services and drinking places increased by 0.6%, while spending at motor vehicle dealerships rose by 0.3%. Meanwhile, sales at electronics and appliance stores declined by 0.4%, suggesting consumers are prioritizing experiences over discretionary purchases.

The Federal Reserve's interest rate hikes have added another layer of financial pressure. With the federal funds rate now in the range of 5.00-5.25%, borrowing costs have risen significantly. The average annual percentage rate (APR) on new credit cards reached 20.65% in May 2023, the highest level since the Federal Reserve began tracking this data in 1994, according to Federal Reserve data.

"Higher interest rates are making debt more expensive for households carrying credit card balances," noted Mark Zandi, chief economist at Moody's Analytics. "This creates a double bind for consumers: prices remain high while the cost of financing purchases increases."

The spending-income gap has significant implications for businesses. Companies in sectors like retail, hospitality, and entertainment may benefit from continued consumer spending in the short term. However, the trend could lead to reduced consumer discretionary spending as households prioritize debt repayment and rebuilding savings.

"Businesses should prepare for potential shifts in consumer behavior," warned Lisa Cook, chief economist at LinkedIn. "As households face increasing financial pressure, we may see a return to more value-conscious shopping patterns and reduced spending on non-essential items."

The economic outlook remains uncertain. While consumer spending has been a key driver of economic growth, the current trend of spending exceeding income growth cannot continue indefinitely. Economists will be watching closely for signs of a potential pullback in consumer spending, which could impact overall economic growth in the coming quarters.

"The American consumer has been remarkably resilient, but there are limits to that resilience," said Diane Swonk, chief economist at KPMG. "The question is not whether consumers will eventually pull back, but when and how sharply that adjustment will occur."

Federal Reserve officials have indicated they will continue to monitor inflation and consumer spending closely as they determine future monetary policy. The central bank's dual mandate of maximum employment and stable prices requires careful balancing as they navigate these conflicting economic signals.

For households, the current environment underscores the importance of financial planning and budgeting. Financial advisors recommend creating emergency funds, reducing high-interest debt, and adjusting spending habits to align with current income levels. The Federal Reserve's consumer financial protection resources offer guidance on managing finances in the current economic climate.

As the economy continues to evolve, the relationship between consumer spending and income growth will remain a critical indicator of financial health and economic stability. The current spending-income gap serves as a reminder of the complex interplay between inflation, wages, and consumer behavior that shapes the economic landscape.

Comments

Please log in or register to join the discussion