An in-depth exploration of how marriage affects tax liabilities in Switzerland, revealing complex patterns across different cantons and implementing an interactive visualization to help voters understand the implications of the upcoming tax initiative.

The upcoming Swiss referendum on marriage taxation represents more than a simple policy choice—it embodies a fundamental question about fairness in how society structures its financial obligations. As citizens prepare to vote on whether married couples should file taxes individually rather than jointly, Guillaume Endignoux provides a meticulous technical examination that transcends political rhetoric to reveal the mathematical reality beneath Switzerland's complex tax architecture.

At its core, the marriage tax question hinges on a simple premise: whether two individuals should pay the same total tax whether they file jointly or separately. The current system, which Endignoux terms "marriage tax," creates situations where couples face financial penalties or benefits based solely on their marital status. This analysis moves beyond anecdotal evidence to quantify these effects systematically.

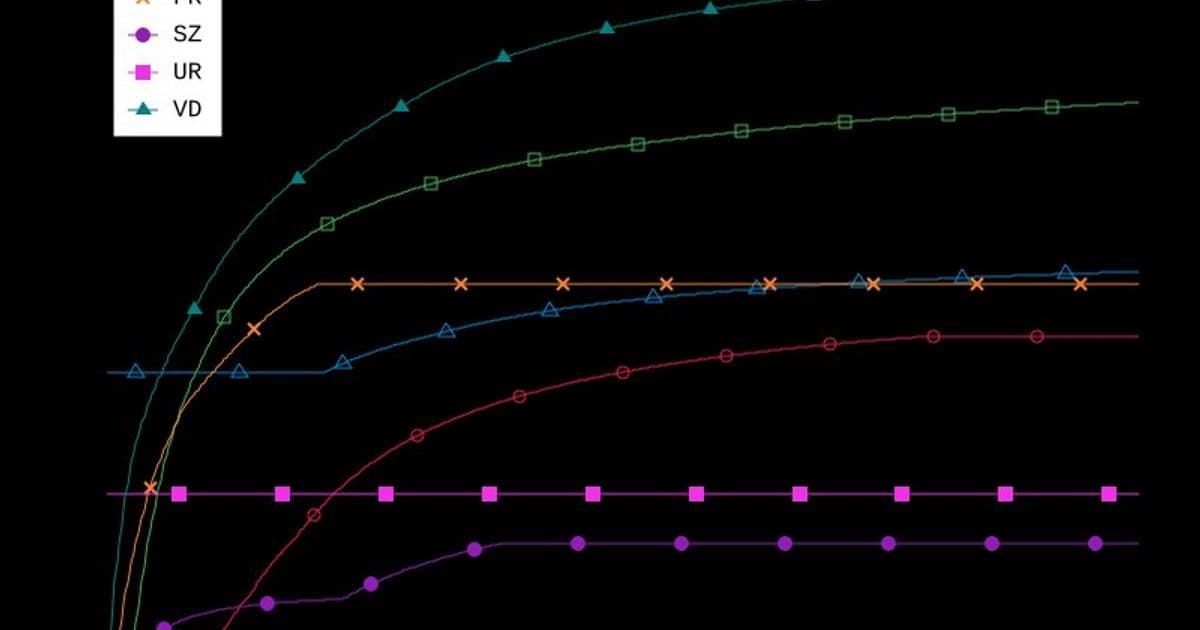

Switzerland's tax system operates at three distinct administrative levels—federal, cantonal, and municipal—creating a complex web of regulations that vary dramatically across the 26 cantons. The federal government establishes baseline tax brackets, while cantons exercise considerable freedom in designing their own approaches. Some cantons implement piecewise linear tax functions with marginal rates applied to income brackets, while others employ more exotic methodologies. Fribourg, for instance, structures its tax progression around average tax rates rather than marginal rates. Obwald and Uri apply flat taxes independent of income levels, and Basel-Landschaft utilizes intricate mathematical formulas that would challenge even seasoned tax professionals.

For married couples, the calculation complexity intensifies. Cantons employ two primary approaches: either establishing separate tax tables for married couples or applying a splitting factor that reduces the couple's combined taxable income before applying standard individual rates. A splitting factor of two would theoretically ensure that couples with equal incomes pay the same total tax whether married or not. However, as Endignoux demonstrates, reality rarely aligns with this theoretical ideal.

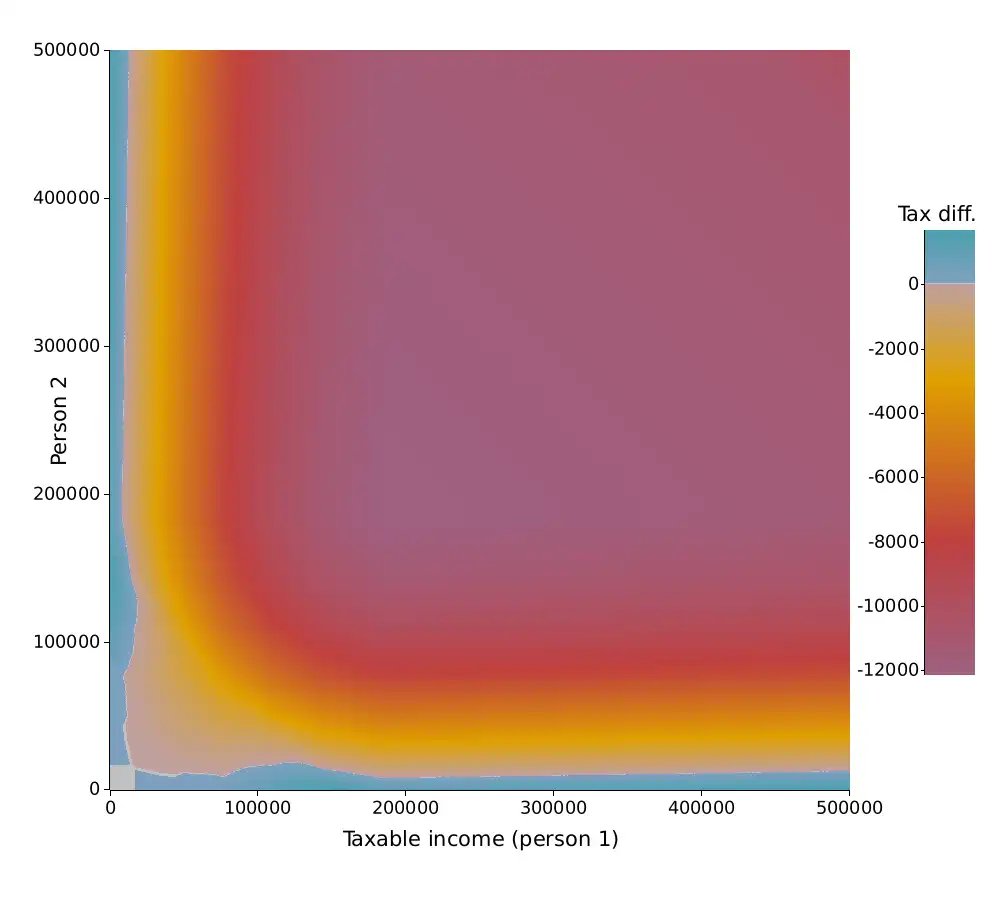

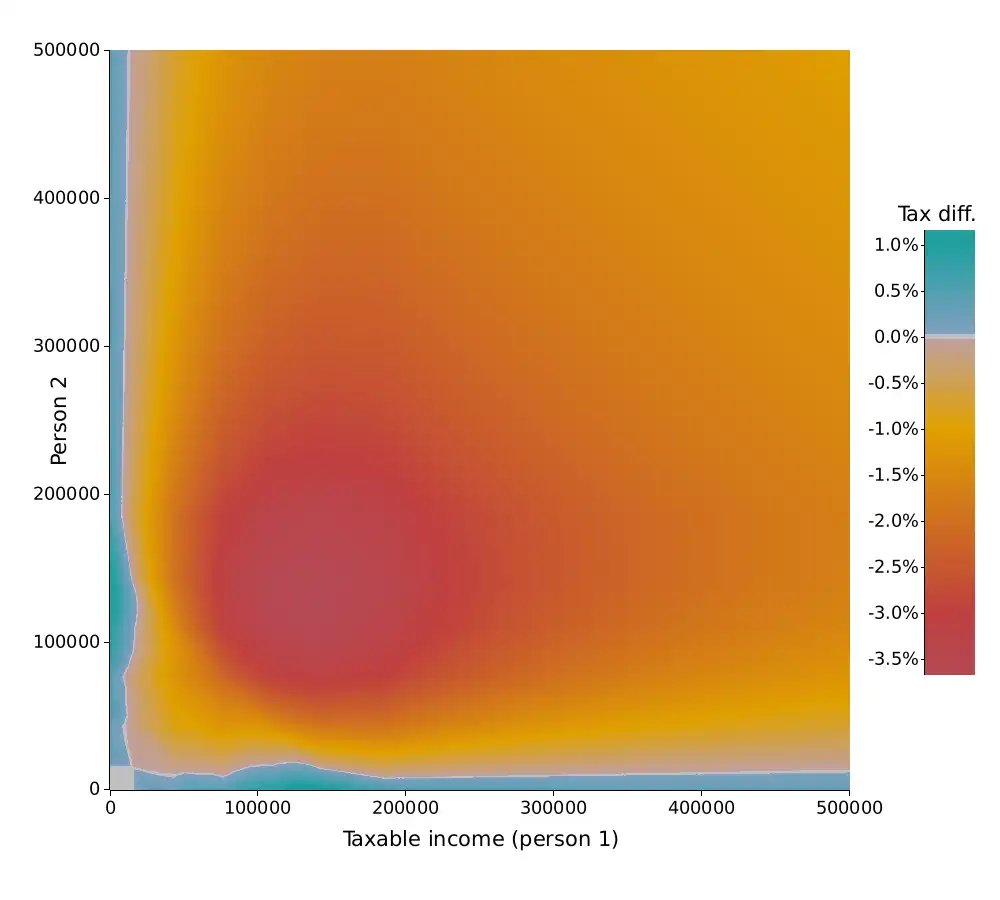

The marriage penalty, mathematically defined as the difference between taxes paid jointly versus separately, reveals striking variations across cantons. At the federal level, a clear disadvantage emerges for couples where both partners earn more than approximately 20,000 CHF annually, with potential penalties reaching 12,000 CHF per year or 3.5% of total income for dual earners between 100,000 and 200,000 CHF. The cantonal picture proves even more diverse.

Effective income tax rate as a function of taxable income in several cantons, 2025

Effective income tax rate as a function of taxable income in several cantons, 2025

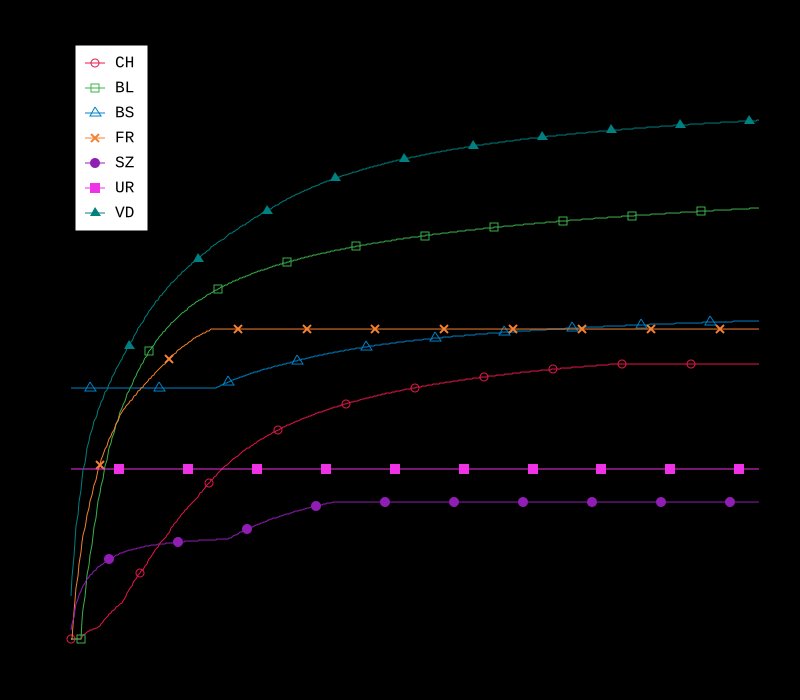

In Zurich and Ticino, the marriage penalty remains relatively modest, capped at around 1% of total income. Fribourg, with its splitting factor of exactly two, creates an interesting equilibrium where couples with equal incomes face no marriage penalty, while those with income disparities experience either benefits or penalties depending on the degree of inequality. The visualization for Fribourg reveals fascinating patterns along the diagonal where incomes are equal, with divergent effects appearing as income disparity increases.

Single and married income tax rate as a function of taxable income in the canton of Fribourg, 2025

Single and married income tax rate as a function of taxable income in the canton of Fribourg, 2025

Perhaps most revealing is the canton of Neuchâtel, which employs a splitting factor slightly below two, creating what Endignoux describes as a "bird-like" pattern in the marriage penalty visualization. Along the main diagonal where partners have similar incomes, couples face a slight additional tax. Those with vastly unequal incomes encounter substantial penalties, while partners with moderate income inequality actually benefit from marriage, paying less tax than they would as individuals. This complex interplay between income equality and tax liability challenges simplistic narratives about marriage taxation.

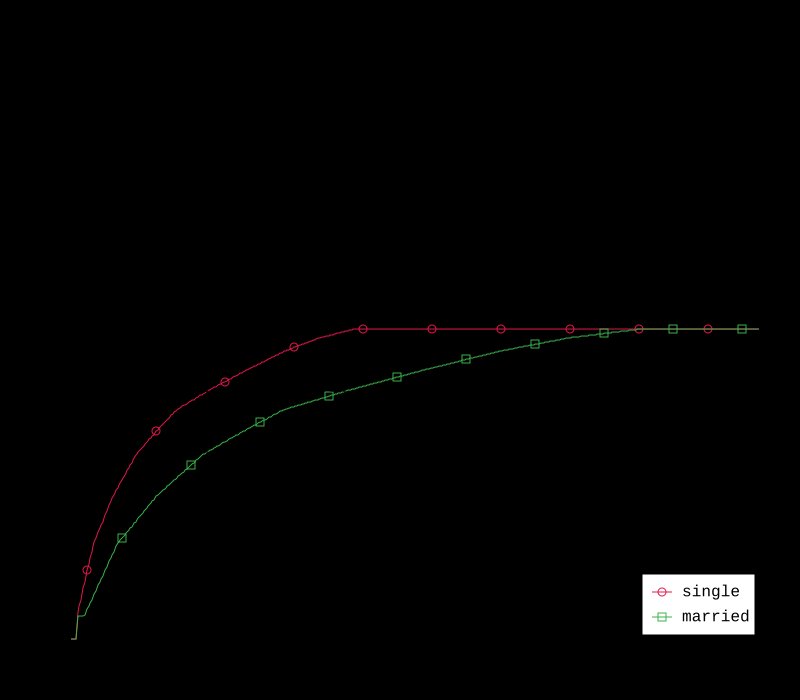

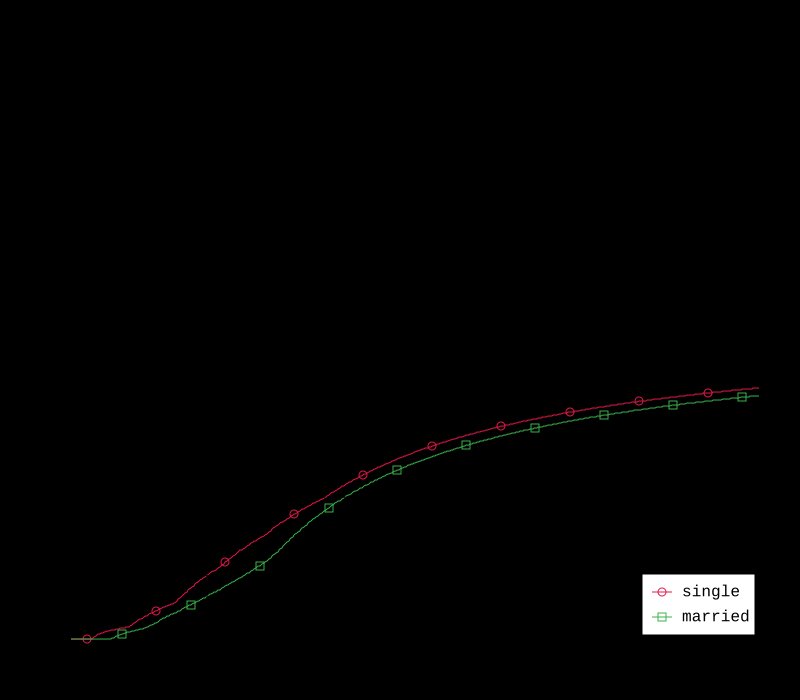

Single and married federal income tax rate as a function of taxable income, 2025

Single and married federal income tax rate as a function of taxable income, 2025

Geneva presents an entirely different scenario, where married couples consistently pay lower cantonal taxes, with potential bonuses exceeding 12,000 CHF annually. The neutral zone along the main diagonal forms an intriguing pattern of aligned squares, suggesting the interaction between tax brackets and the splitting mechanism creates unexpected mathematical regularities.

2D color plot of the federal marriage tax difference

2D color plot of the federal marriage tax difference

Endignoux's methodology deserves particular attention. Faced with the challenge of obtaining machine-readable tax data from natural language legal documents and scattered PDF tables, the author developed an automated system to extract information from the Federal Tax Administration's online calculator. This approach, while innovative, highlights a broader issue: the opacity of tax data in a digital age. Citizens should have ready access to the mathematical foundations of tax laws, especially when voting on changes to those laws.

The technical implementation showcases sophisticated programming techniques. Using Rust for data processing and WebAssembly for the interactive visualization, Endignoux created a performant system that allows users to explore different scenarios across cantons and income levels. The WASM module, optimized to just 72KB after compression, demonstrates how complex computational tasks can be delivered efficiently to web browsers.

2D color plot of the federal marriage tax difference

2D color plot of the federal marriage tax difference

These findings carry significant implications for voters. The marriage tax is not a monolithic phenomenon but a complex interplay of local tax policies, income distribution, and mathematical formulations. What benefits one couple in one canton may penalize another couple in a different jurisdiction. The referendum, framed as a simple choice between joint and individual filing, actually touches upon deeper questions about tax fairness, income equality, and the role of marriage in economic policy.

Counter-perspectives deserve consideration. The current system may reflect deliberate policy choices rather than mere mathematical artifacts. Some cantons might intentionally structure tax systems to encourage or discourage marriage based on broader social objectives. The splitting factor approach, while creating apparent penalties for some couples, might actually simplify tax administration or reduce opportunities for tax avoidance that joint filing could enable.

Moreover, this analysis focuses narrowly on income tax for childless couples. Real-world tax calculations involve additional complexities—wealth taxes, deductions for children, dependent relatives, and various social benefits—that could significantly alter the marriage penalty calculations. The author appropriately acknowledges these limitations while suggesting that the revealed patterns provide valuable general insights.

As Swiss citizens prepare to vote, Endignoux's work offers a rare example of how technical analysis can illuminate policy debates. By moving beyond anecdotes to quantify effects systematically, the analysis provides a foundation for more informed decision-making. The interactive visualization allows voters to explore scenarios relevant to their personal circumstances, transforming abstract policy into concrete financial implications.

The broader lesson extends beyond Swiss borders. As societies grapple with questions about tax fairness and family policy, technical approaches like this one can help separate political rhetoric from mathematical reality. In an era where policy debates often devolve into simplified narratives, such careful analysis reminds us that tax systems—like the families they affect—are complex systems where small changes can produce unexpected and sometimes counterintuitive outcomes.

Comments

Please log in or register to join the discussion