Global smartphone shipments to fall 13% in 2026 due to memory shortage, with low-end Android vendors hit hardest while Apple and Samsung gain market share.

The global smartphone market is bracing for its most severe downturn ever, with shipments projected to plummet 13% in 2026 to just 1.12 billion units—the lowest annual volume in over a decade. This dramatic decline, revealed in IDC's latest Worldwide Quarterly Mobile Phone Tracker, represents a stark reversal from previous forecasts and signals a fundamental restructuring of the entire mobile industry.

Memory Shortage Triggers Industry-Wide Crisis

The crisis stems from a memory supply chain disruption that IDC analysts describe as a "tsunami-like shock" spreading across consumer electronics. Unlike typical market fluctuations, this shortage has exposed deep vulnerabilities in smartphone manufacturing, particularly affecting Android vendors concentrated in the low-end segment.

Francisco Jeronimo, IDC's vice president for Worldwide Client Devices, explains the severity: "What we are witnessing is not a temporary squeeze, but a tsunami-like shock originating in the memory supply chain, with ripple effects spreading across the entire consumer electronics industry."

The impact varies dramatically by vendor positioning. Low-end manufacturers face an existential threat as rising component costs squeeze already thin margins. These companies have limited options—either absorb losses or pass increased costs to consumers, potentially pricing them out of the market entirely.

Winners and Losers in the New Landscape

Apple and Samsung emerge as the relative winners in this crisis. Their premium positioning and stronger margins provide a buffer against component cost increases. More importantly, their ability to maintain profitability at higher price points positions them to potentially expand market share as weaker competitors struggle.

"As smaller and low-end-positioned Android vendors struggle with rising costs, Apple and Samsung could not only weather the storm but potentially expand market share as the competitive landscape tightens," Jeronimo notes.

This dynamic could accelerate existing market consolidation trends, with smaller players either exiting the market or being acquired by larger competitors.

Structural Changes Beyond Temporary Decline

Nabila Popal, senior research director with IDC's Worldwide Quarterly Mobile Phone Tracker, emphasizes that this crisis represents more than a temporary setback. "The memory crisis will cause more than a temporary decline; it marks a structural reset of the entire market, fundamentally reshaping long-term TAM (Total Addressable Market), the vendor landscape, and the product mix."

The market is experiencing a fundamental shift in its economic structure. Smartphone Average Selling Prices (ASP) are projected to rise 14% to a record $523 in 2026, even as unit volumes collapse. This price increase reflects both component cost pressures and a strategic shift away from the most price-sensitive market segments.

The End of the Sub-$100 Smartphone

Perhaps most significantly, the crisis appears to be permanently eliminating the sub-$100 smartphone segment, which represented 171 million devices in previous years. Memory prices are expected to stabilize by mid-2027 but won't return to previous levels, making ultra-low-cost devices economically unviable.

"There is no return to business as usual for vendors and consumers," Popal states. This represents a fundamental reset in how smartphones are manufactured and sold globally.

Regional Variations in Impact

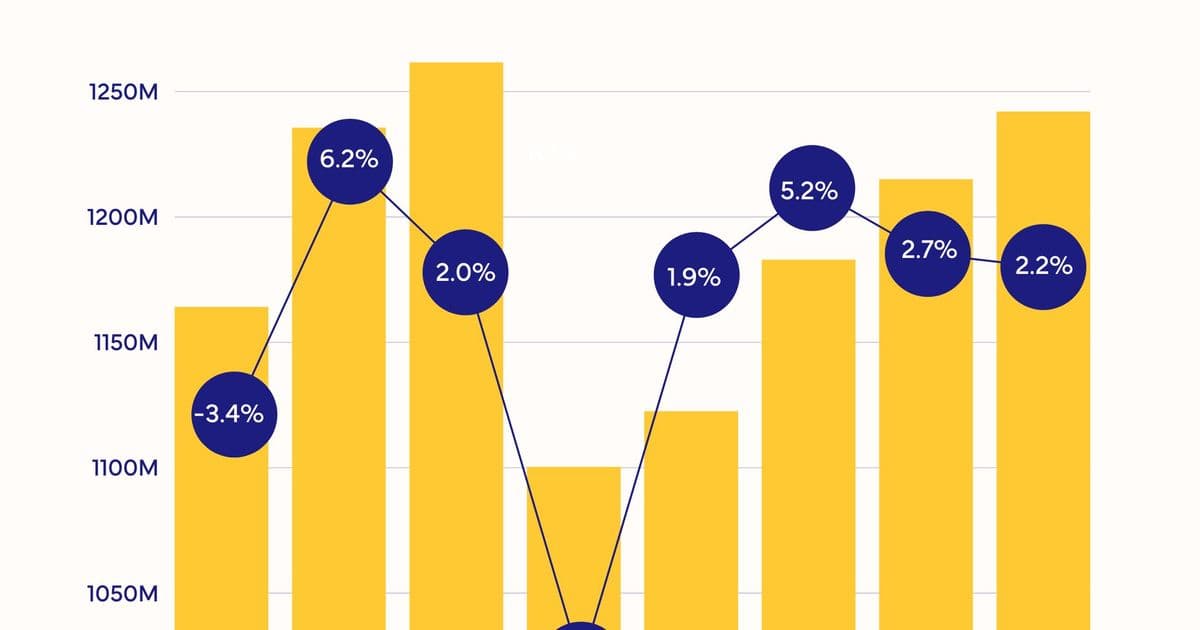

The crisis affects regions differently based on their market composition. Markets with high concentrations of low-end smartphones face the steepest declines. The Middle East and Africa region is forecast to experience the sharpest drop at 20.6% year-over-year, while China and Asia Pacific (excluding Japan and China) are expected to decline 10.5% and 13.1%, respectively.

Recovery Timeline and Long-Term Outlook

IDC projects a modest 2% recovery in 2027 as memory prices stabilize, followed by a stronger 5.2% year-over-year rebound in 2028. However, this recovery will occur in a fundamentally different market structure than existed before the crisis.

The smartphone industry appears to be entering a new era characterized by:

- Higher average prices and fewer low-end options

- Increased market concentration among premium vendors

- Reduced total addressable market size

- More sustainable but less accessible pricing models

This transformation mirrors broader trends in consumer electronics, where component shortages and supply chain vulnerabilities have exposed the fragility of ultra-low-cost manufacturing models. The smartphone market's response—consolidation, price increases, and exit from unprofitable segments—may become a template for other consumer technology sectors facing similar pressures.

For consumers, the implications are clear: fewer choices at the low end, higher prices across the board, and a market increasingly dominated by premium brands. For the industry, the crisis represents both a painful contraction and an opportunity to build more sustainable business models less vulnerable to supply chain shocks.

The smartphone market's journey through this crisis will be closely watched as a case study in how technology industries adapt to fundamental supply constraints and whether the era of ever-cheaper devices has reached its natural limit.

Comments

Please log in or register to join the discussion