SpaceX’s first trading day was less a normal IPO than a repricing event for the commercial space economy, with public investors assigning software-like multiples to rockets, satellites, defense contracts, and Starlink cash flow.

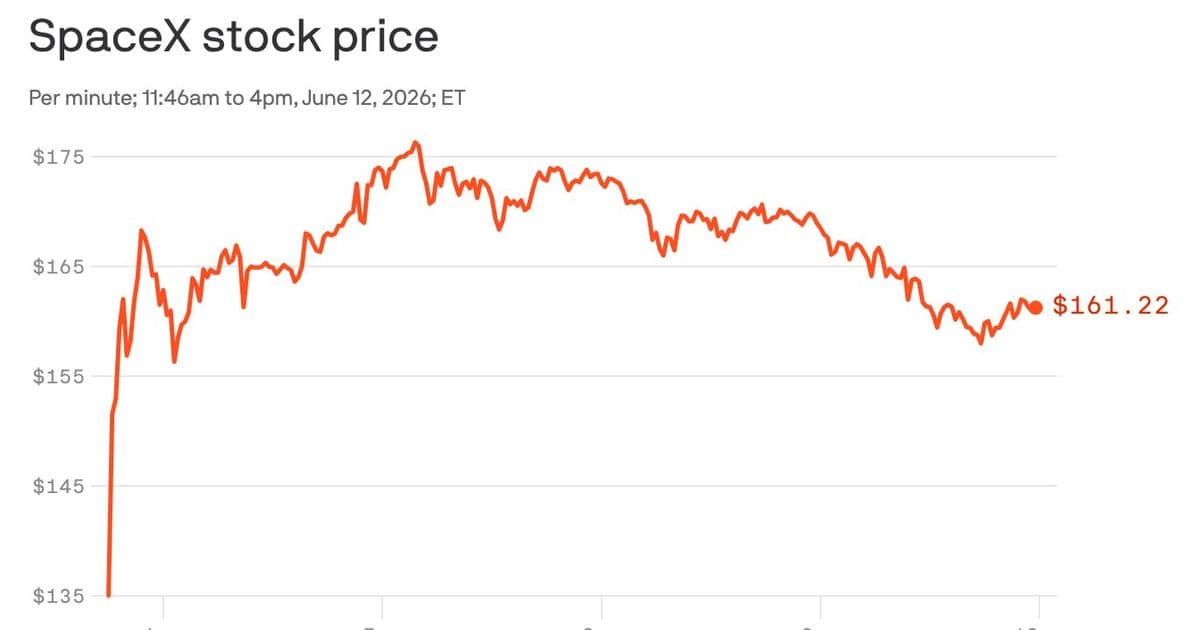

SpaceX closed its first day of public trading 19% above its IPO price, giving Elon Musk’s rocket and satellite company a market value of about $2.1 trillion and placing it among the largest publicly traded companies in the United States. According to Axios, shares were priced at $135 before trading began and finished the session at $160.95, a gain that turned an already record-size offering into one of the clearest signals yet that public markets are willing to pay extreme prices for strategic technology infrastructure.

The offering raised roughly $75 billion and valued SpaceX at about $1.77 trillion at the IPO price. By the close, the company’s equity value had moved past the $2 trillion mark. That is not just a headline number. It means investors are treating SpaceX less like a traditional aerospace manufacturer and more like a platform company sitting at the intersection of launch services, satellite broadband, national security, communications infrastructure, and eventually space logistics.

The valuation is the central story. Axios reported that SpaceX entered the market at roughly 90 times sales. At a $2.1 trillion closing value, that multiple implies revenue in the low-$20-billion range if measured against the same sales base. That is an extraordinary price for any industrial company, even one with dominant launch share and a fast-growing satellite internet unit. For comparison, mature aerospace and defense contractors usually trade on earnings, backlog, and cash conversion. SpaceX is being priced on optionality: the probability that its current businesses become the base layer for several future markets.

The public-market debut also changes the strategic clock for SpaceX. As a private company, SpaceX could fund long-term projects through private rounds, internal cash generation, customer deposits, and government contracts while keeping financial disclosures limited. As a public company, it will face a quarterly investor base that wants clearer answers on Starlink profitability, launch margins, capital expenditure, debt, free cash flow, and the cost of developing Starship. That tension is now part of the investment case.

SpaceX’s core business has three major valuation pillars. The first is launch, where the company’s reusable Falcon 9 system reshaped industry pricing and cadence. The second is Starlink, the satellite broadband network that gives SpaceX a recurring consumer, enterprise, maritime, aviation, and government revenue stream. The third is Starship, the heavy-lift vehicle program described on SpaceX’s official site as central to future missions beyond Earth orbit. Public investors are effectively paying today for the chance that those three assets compound into a vertically integrated space infrastructure company.

That is why the 19% first-day move matters. IPO pops are often treated as trading theater, but in this case the move reset the implied cost of capital for the space sector. A $2.1 trillion SpaceX can use equity as a strategic weapon. It can fund satellite deployments, manufacturing capacity, launch infrastructure, acquisitions, employee compensation, and large research programs with a currency that now has deep public-market liquidity. Competitors in launch, satellite broadband, defense technology, and telecom will be measured against that balance-sheet advantage.

The market context is also favorable to premium technology listings. Investors have spent the past several years rewarding companies tied to artificial intelligence infrastructure, cloud computing, chips, defense autonomy, and high-scale data networks. SpaceX fits that risk appetite even though its hardware profile is capital intensive. Starlink connects directly to communications demand. Launch connects to defense and commercial space expansion. Starship connects to a long-duration story that gives the stock a narrative premium, even if near-term cash flows do not yet justify the multiple in conventional terms.

That premium comes with obvious risk. A 90-times-sales valuation leaves little room for execution errors. Rocket programs can slip. Satellite networks require constant capital spending. Consumer broadband markets are competitive. Government contracts can be politically sensitive. International operations can face spectrum, licensing, and security restrictions. Starship, the highest-upside asset, is also the least predictable from a timing and cost perspective. If revenue growth slows or margins disappoint, the stock could re-rate sharply because the valuation assumes years of expansion before those earnings fully arrive.

The lock-up period is the next market pressure point. Early employees, venture investors, and insiders may eventually gain the ability to sell portions of their holdings, increasing float and testing demand beyond the first-day scarcity effect. For a company that has created significant paper wealth over more than two decades, the end of selling restrictions could introduce volatility. The first day showed demand. The lock-up expiration will show how much of that demand can absorb real supply.

The IPO also has implications for Tesla. Musk’s public-company portfolio is now anchored by two giant equities with different business models but overlapping investor bases. Tesla is an electric vehicle, energy storage, autonomy, and robotics story. SpaceX is a launch, satellite, communications, and defense-adjacent infrastructure story. Some investors will view them as complementary expressions of the same founder-led industrial technology thesis. Others will worry about governance, capital allocation, executive attention, and whether public-market pressure around SpaceX adds another layer of complexity to Musk’s broader empire.

For the wider technology market, SpaceX’s debut may become a pricing reference for other late-stage private companies. If investors can absorb a $75 billion IPO and still bid the stock up 19%, bankers will see a stronger opening for large AI, defense technology, and infrastructure software listings. Companies such as AI model developers, data center suppliers, autonomous systems vendors, and cybersecurity platforms will read the signal carefully. Public investors are still selective, but they are willing to write very large checks for companies viewed as strategic infrastructure.

The strategic question is whether SpaceX can translate its technical lead into public-company financial discipline. Launch dominance alone would not normally support a multi-trillion-dollar valuation. The bull case depends on Starlink becoming a high-margin global network, launch demand continuing to rise, national security work expanding, and Starship opening new markets that are not yet fully reflected in revenue. The bear case is simpler: the company is already priced as if much of that future has arrived.

What changed on the first day of trading is that SpaceX moved from private-market legend to public-market benchmark. Its financial statements, capital needs, margins, and execution timelines will now be measured against a $2.1 trillion equity value. That creates pressure, but it also gives the company unusual strategic flexibility. The market is no longer debating whether SpaceX is an important technology company. It is debating how much of the future space economy investors have already paid for.

Comments

Please log in or register to join the discussion