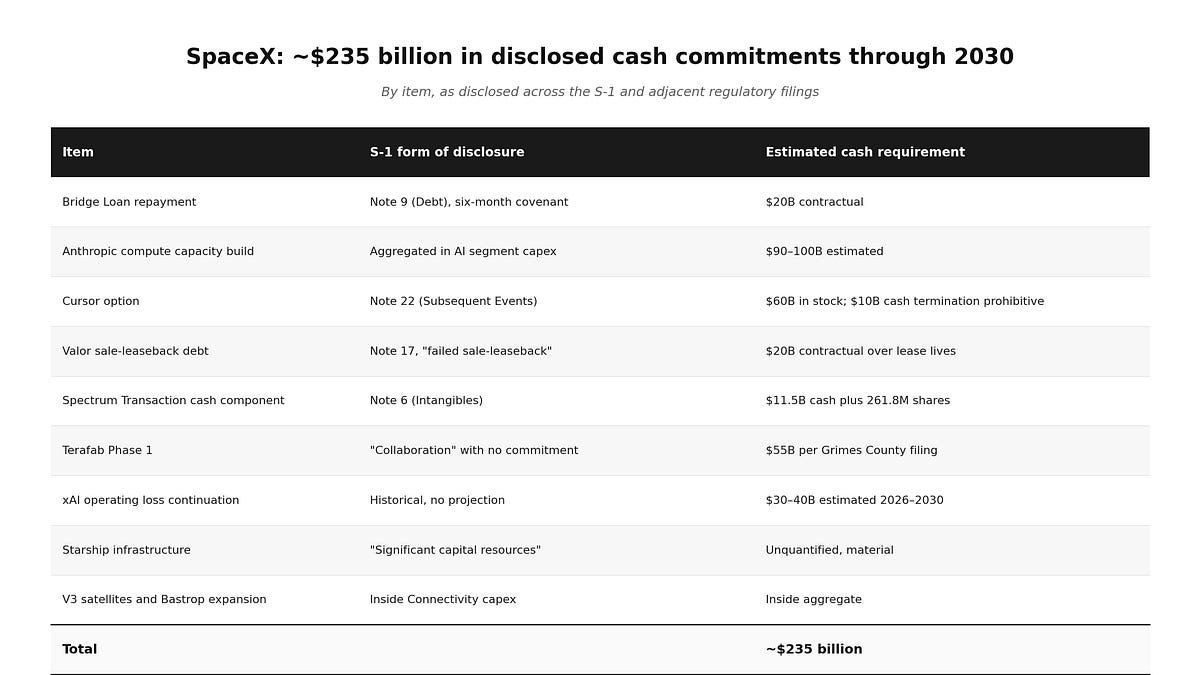

SpaceX’s filing for a public offering lists roughly $235 billion of cash commitments through 2030, yet the IPO is expected to raise only $50‑75 billion. The gap stems from debt repayment, long‑term AI contracts, a forced acquisition option, and large infrastructure projects that are disclosed in separate notes without aggregation. This analysis breaks down the individual items, shows why the gap is larger than the headline raise, and explains the practical limits on how SpaceX could close it.

What the filing claims

- SpaceX’s S‑1 (filed May 20, 2026) lists ≈ $235 billion in cash commitments through 2030, covering debt repayment, AI service contracts, capex for data‑center expansion, a $60 billion stock‑based acquisition option (Cursor), and several large‑scale projects such as the Terafab‑Tesla collaboration.

- The IPO is expected to bring $50‑75 billion gross, of which roughly $20 billion must be used immediately to retire a bridge loan.

- After underwriting fees and the bridge‑loan repayment, the net cash available from the offering is $30‑50 billion.

- The filing repeatedly warns that “capital requirements are significant and ongoing” but never aggregates the disclosed commitments into a single cash‑flow picture.

What’s actually new in the filing

| Item | Cash impact (USD) | Timing | Where it appears in the S‑1 |

|---|---|---|---|

| Bridge loan repayment | $20 B (mandatory) | Within 6 months of closing | Debt footnote |

| Anthropic AI contract | $1.25 B/mo through May 2029 (cancellable) | Ongoing | Revenue schedule, but capex for GPUs is hidden in AI‑segment capex ($12.7 B for 2025, $7.7 B Q1 2026) |

| Cursor acquisition option | $60 B in Class A stock (equity dilution) + $10 B cash termination fee | Call window opens 7 days after IPO, expires Oct 2026 | “Option Mechanics” note |

| Terafab Phase 1 (Tesla collab) | $55 B (Phase 1) – $119 B full build‑out | Filed May 6, 2026 (tax‑abatement) | Separate county filing, not in S‑1 capex table |

| Spectrum sale‑leaseback | $19.6 B total, $11.5 B cash component | Closing Nov 2027 | “Intangible asset acquisition” note |

| Valor related‑party lease | $3.4 B/yr lease payments | Ongoing | “Failed sale‑leaseback” classification |

| Litigation & regulatory exposures | $0.4‑0.5 B disclosed, plus unquantified risk | Ongoing | Risk‑factors narrative |

The numbers above are each correct in their own section, but the S‑1 never adds them together. When expressed in a single currency, the total known cash outflow through 2030 is roughly $235 billion.

Why the gap matters

- Net IPO proceeds: $30‑50 billion after fees and the mandatory bridge‑loan repayment.

- Cash‑flow reality: As of the March 31, 2026 balance sheet, SpaceX held $15.85 billion in cash and $7.82 billion in marketable securities. Its free‑cash‑flow run‑rate was ‑$36 billion per year.

- Gap size: $235 billion (commitments) – $40 billion (mid‑point net IPO) ≈ $195 billion shortfall, or about 3‑5× the amount raised.

- Strategic implications: The forced Cursor acquisition is effectively a cash‑conserving move. Exercising the option uses newly‑issued equity (dilution) rather than the $10 billion cash termination fee that the balance sheet cannot comfortably cover. The option’s timing (stock‑price set at IPO valuation) forces the first major use of the equity before the market can test the valuation.

Limitations and realistic financing paths

- Tesla cash infusion – Speculation suggests a possible $45 billion cash injection from a Tesla‑SpaceX merger. Even if realized, it would cover only a fraction of the $235 billion gap.

- Additional equity offerings – The IPO creates a tradable currency, but each follow‑on raise would further dilute existing shareholders and likely be priced at a discount if cash‑flow remains negative.

- Related‑party debt – The Valor lease‑back and other private‑capital structures could be scaled, but they increase leverage and governance risk without adding new cash.

- Government contracts – The filing does not contain any disclosed CHIPS‑Act or other federal funding that could materially shrink the gap.

- Operational cash‑flow improvement – Turning a ‑$36 billion free‑cash‑flow into a positive number would require massive revenue growth (e.g., scaling the Anthropic contract) and simultaneous capex financing, which the S‑1 does not quantify.

In short, the S‑1 provides the ingredients for a $235 billion cash‑requirement pie, but it leaves the crucial question unanswered: where will the extra cash come from? The only concrete source is the IPO itself, which falls dramatically short.

Bottom line for investors and boards

- The filing is internally consistent; each note is correct in isolation.

- The lack of aggregation means a reader must do the heavy lifting to see the full exposure.

- The forced acquisition option and the bridge‑loan repayment create a near‑inevitable equity‑dilution event shortly after the IPO.

- Without a clear, disclosed financing plan—whether via a Tesla merger, massive secondary offerings, or unprecedented government subsidies—the company faces a structural cash shortfall that could pressure its balance sheet and governance.

Investors should treat the $50‑75 billion raise as a headline number, not a solution to the underlying $235 billion commitment stack. The risk factors section hints at the problem, but the financial statements do not quantify it, leaving a material information gap that any thorough due‑diligence process must fill.

For the full set of numbers and source filings, see SpaceX’s S‑1 (SEC EDGAR), the Grimes County tax‑abatement filing, and the Bridge‑Loan agreement.

Comments

Please log in or register to join the discussion