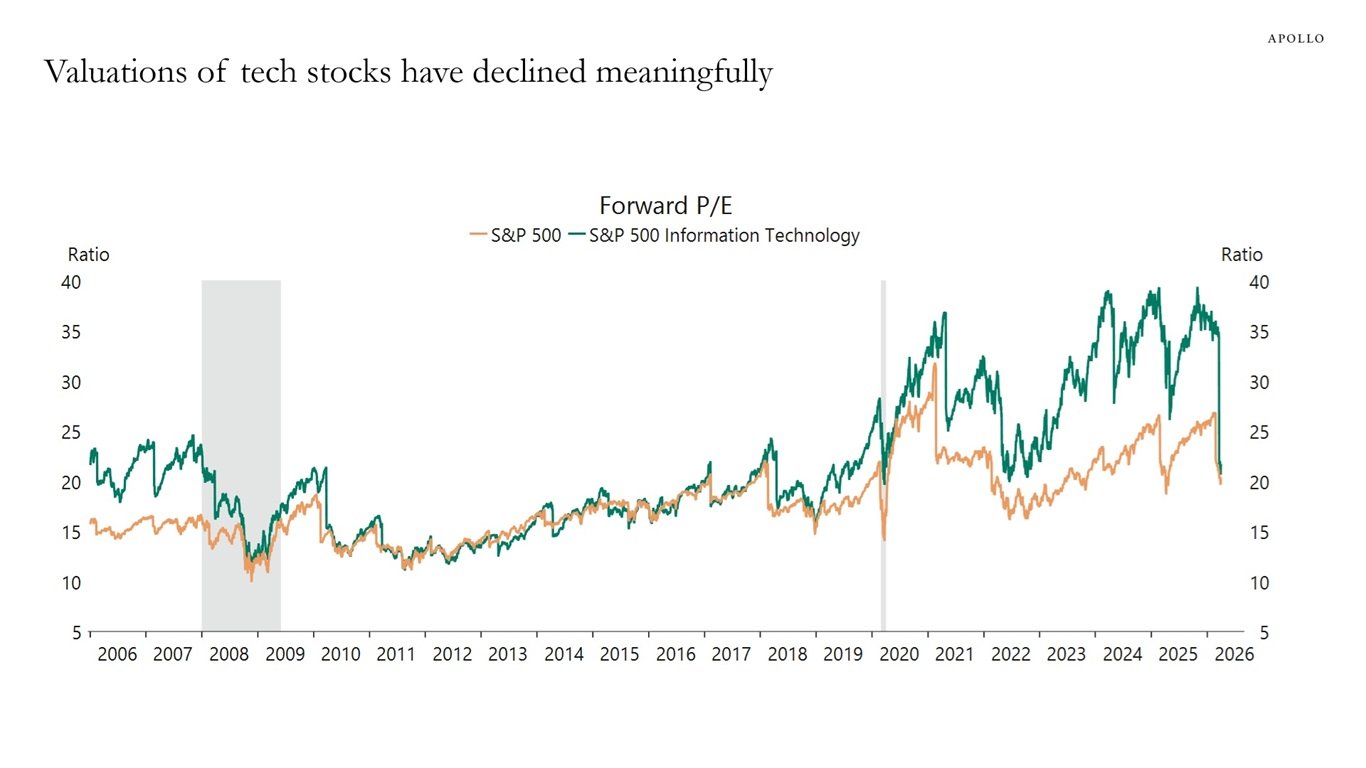

The S&P 500 Information Technology sector's forward P/E ratio has compressed from 40x to 20x, returning to levels last seen before the AI boom began, according to Apollo Chief Economist data.

The tech sector's valuation bubble appears to have definitively burst, with forward price-to-earnings ratios for the S&P 500 Information Technology sector compressing from 40x to 20x over the past year, returning to levels last seen before the AI investment frenzy began in 2023.

This dramatic valuation compression reflects a broader market correction that has hit even the largest technology companies. The ten largest constituents in the S&P 500 Information Technology index have all seen their valuations reset:

- NVIDIA Corp

- Apple Inc

- Microsoft Corp

- Broadcom Inc

- Oracle Corp

- Micron Technology Inc

- Palantir Technologies Inc

- Advanced Micro Devices Inc

- Cisco Systems Inc

- Applied Materials Inc

The data, compiled by Apollo Chief Economist using Bloomberg and Macrobond sources, shows that tech valuations have declined meaningfully from their peak during the AI boom. At 40x forward earnings, the sector was trading at twice the valuation of the broader S&P 500, reflecting investor enthusiasm for AI-related growth prospects.

The data, compiled by Apollo Chief Economist using Bloomberg and Macrobond sources, shows that tech valuations have declined meaningfully from their peak during the AI boom. At 40x forward earnings, the sector was trading at twice the valuation of the broader S&P 500, reflecting investor enthusiasm for AI-related growth prospects.

This correction appears to be more than just a temporary pullback. The return to pre-AI boom valuation levels suggests that market participants have reassessed the timeline and magnitude of AI-driven revenue growth. While AI adoption continues to expand across industries, the immediate revenue impact appears to be taking longer to materialize than investors initially anticipated.

The compression in valuations comes amid broader macroeconomic uncertainty, including persistent inflation concerns, interest rate volatility, and questions about the sustainability of current profit margins in the tech sector. Companies that were trading at premium multiples based on expected AI-driven growth have faced increased scrutiny as investors demand more concrete evidence of revenue acceleration.

This valuation reset could have significant implications for the tech sector's M&A activity, R&D spending, and hiring patterns. Companies that expanded aggressively during the AI boom may need to adjust their growth strategies as access to cheap capital becomes more constrained and valuation multiples normalize.

The return to pre-AI boom valuation levels doesn't necessarily signal the end of technological innovation or AI adoption. Rather, it suggests a more measured approach to valuing growth prospects in an environment where interest rates remain elevated and economic growth faces headwinds. The market appears to be demanding more tangible evidence of AI's impact on the bottom line before assigning premium valuations to technology companies.

The next phase for the tech sector will likely focus on demonstrating how AI investments translate into sustainable revenue growth and improved profit margins, rather than trading on speculative future potential alone.

Comments

Please log in or register to join the discussion