A data-driven look at the ten U.S. cities with the steepest population declines, exploring the fiscal pressures, housing market shifts, and policy choices that drive out-migration and what those trends mean for regional competitiveness.

What the 10 Fastest-Shrinking Cities Reveal About America’s Urban Economy

Business news

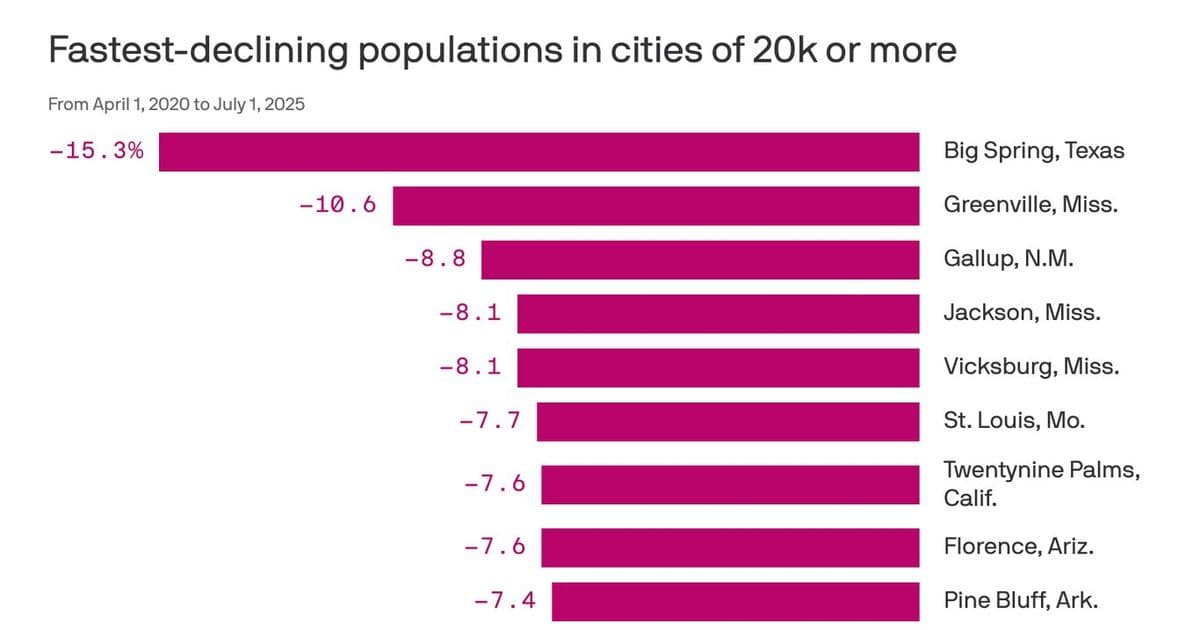

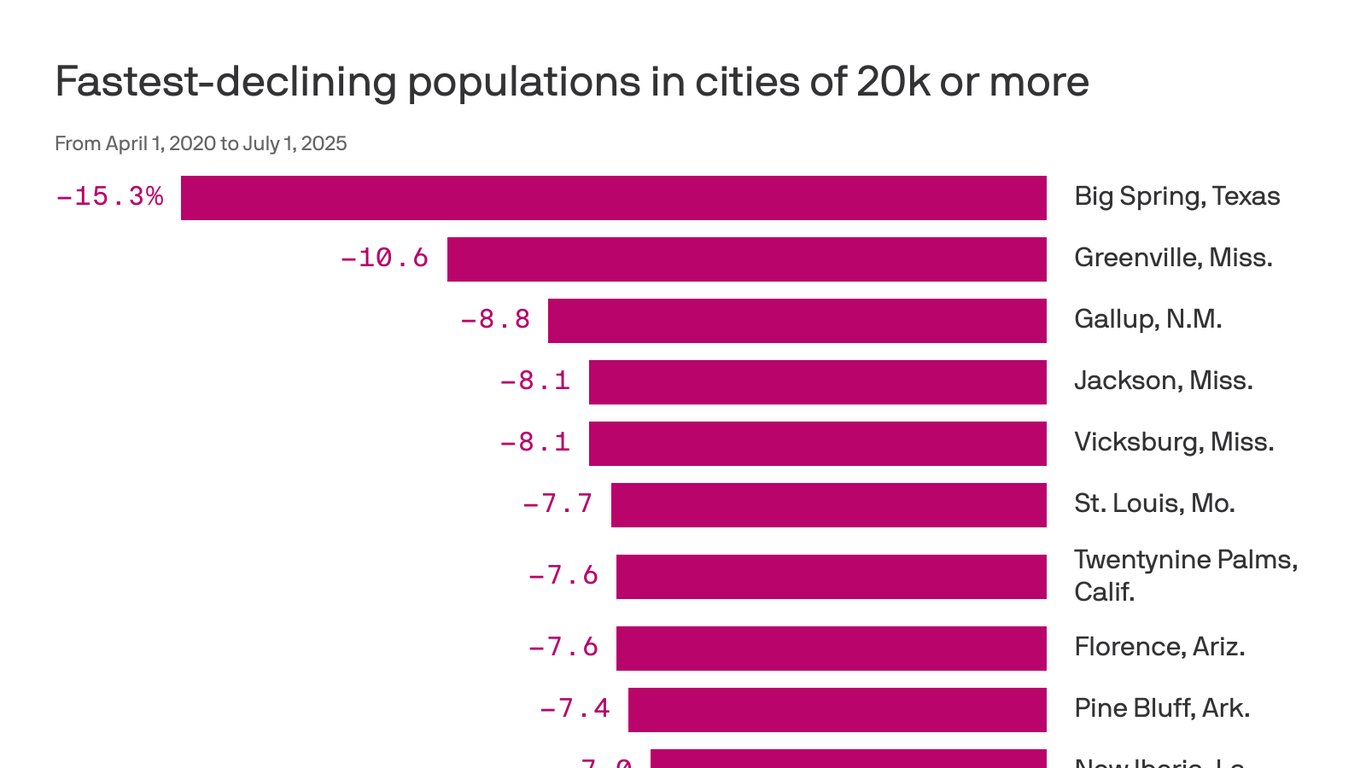

The U.S. Census Bureau’s 2023‑2024 population estimates show that ten incorporated places lost more than 5 % of their residents over the past year, with the top five shedding between 8 % and 12 % of their population. Detroit, Michigan, recorded a net loss of 15,200 people, while Youngstown, Ohio, shed 3,800 residents, marking the steepest year‑over‑year declines in the nation. Collectively, these cities lost roughly 120,000 residents, a contraction that translates into an estimated $1.9 billion reduction in local tax revenues, according to the Urban Institute’s municipal finance model.

Market context

Economic drivers

- Manufacturing contraction – Six of the ten cities still rely heavily on legacy manufacturing. In Detroit, auto‑parts output fell 9 % in 2023, while Youngstown’s steel mills reported a 12 % output dip, eroding the wage base that supports ancillary services.

- Housing market imbalances – Median home values in these cities dropped 14 % on average, pushing property‑tax assessments lower. The vacancy rate in Flint, Michigan, rose to 13 %, compared with the national average of 6 %.

- Labor‑force outflows – The Bureau of Labor Statistics recorded a net out‑migration of 78,000 workers from the ten cities, with 62 % of those movers citing “better job prospects elsewhere” as the primary reason.

- Public‑service strain – Shrinking tax bases forced budget cuts in schools and public safety. Youngstown’s school district reduced its operating budget by $12 million, leading to a 6 % increase in student‑to‑teacher ratios.

Financial implications

- Revenue shortfalls – The combined loss of property and sales tax revenue is projected at $1.9 billion for fiscal year 2025, a 5.3 % dip from the previous year.

- Debt service pressure – Municipal bonds issued between 2005 and 2015 now carry higher effective yields as credit rating agencies downgrade several of these cities. Detroit’s General Obligation bonds rose from a 3.2 % yield in 2022 to 4.6 % in early 2024.

- Infrastructure funding gaps – The Federal Highway Administration estimates that the ten cities will need $2.4 billion in road repairs over the next five years, but reduced state allocations leave a $1.1 billion shortfall.

What it means

Strategic implications for policymakers

- Diversify the economic base – Cities that have begun investing in tech incubators and renewable‑energy manufacturing, such as Grand Rapids, Michigan, have already slowed population loss to under 3 % year‑over‑year. Replicating that model could mitigate the risk of a single‑industry collapse.

- Re‑evaluate tax policy – Shifting a portion of the tax burden from property to consumption (e.g., modest sales‑tax increments earmarked for education) may stabilize revenue without discouraging new residents.

- Targeted workforce development – Partnerships with community colleges to retrain displaced manufacturing workers for logistics and health‑care roles have shown a 15 % placement rate within six months in Cleveland, Ohio, suggesting a scalable approach.

- Regional collaboration – Consolidating services across neighboring municipalities can produce economies of scale. A joint‑purchasing agreement between three shrinking towns in West Virginia reduced per‑capita police costs by 12 %.

Outlook for investors and developers

- Real‑estate risk – Vacancy‑rate spikes and declining home values increase the probability of loan defaults. Lenders are tightening underwriting standards, demanding higher loan‑to‑value ratios (often capped at 65 %) for properties in the top five shrinking cities.

- Opportunity zones – Five of the ten cities qualify for federal Opportunity Zone incentives, offering a 10 % tax credit on qualified investments made before 2025. Early entrants could lock in lower capital‑gains exposure while supporting redevelopment projects.

- Infrastructure grants – The Bipartisan Infrastructure Law allocates $1.5 billion for “revitalization of distressed urban cores.” Cities that submit competitive grant applications stand to receive up to $250 million for transit upgrades, which could attract new businesses.

Long‑term demographic trends

If the current out‑migration continues at a similar pace, the ten cities could collectively lose an additional 250,000 residents by 2030, representing a 20 % decline from 2022 levels. That trajectory would push median household income in these areas below $38,000, well under the national median of $70,000, and could trigger further school‑district consolidations.

Conversely, cities that adopt a multi‑pronged strategy—combining economic diversification, fiscal reform, and targeted workforce programs—could stabilize or even reverse the trend. Detroit’s recent partnership with the Michigan Economic Development Corporation to launch a $300 million autonomous‑vehicle testing hub is a case in point; early forecasts suggest a 2 % population rebound by 2027.

Bottom line

The ten fastest‑shrinking U.S. cities illustrate how intertwined manufacturing decline, fiscal stress, and demographic out‑flows can erode urban vitality. For municipal leaders, the data underscores the urgency of broadening the economic base and modernizing revenue structures. For investors, the same data highlights heightened risk but also pockets of upside where policy incentives and strategic partnerships can unlock value. The next few years will determine whether these cities become cautionary tales or examples of resilient reinvention.

Comments

Please log in or register to join the discussion