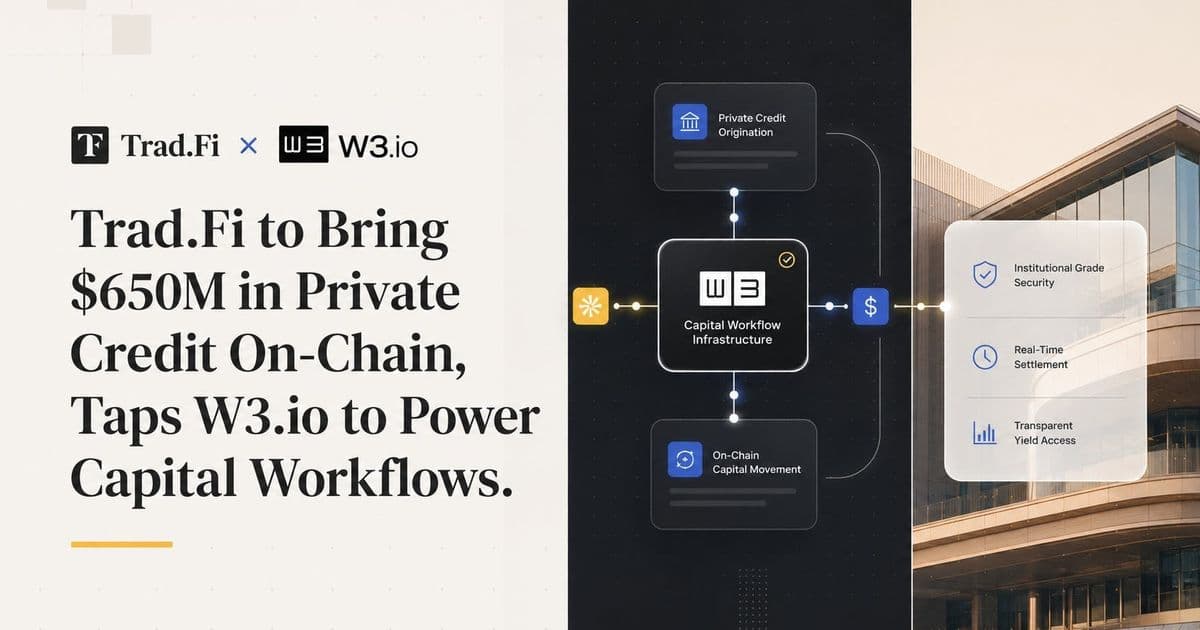

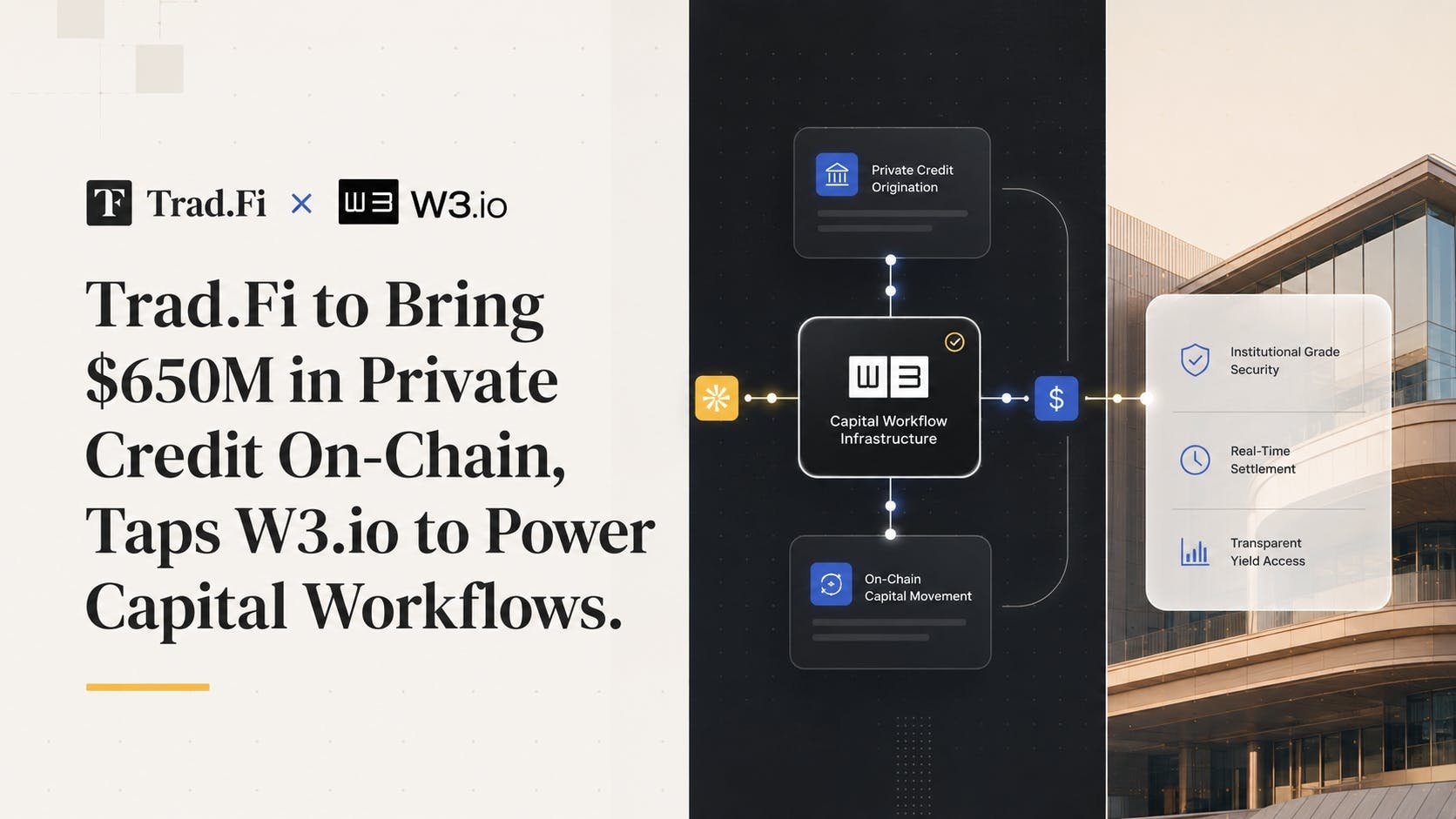

Trad.Fi says it will tokenize $650 million in private credit and route the operational plumbing through W3.io. The number is large, the category is crowded, and the real question is whether on-chain rails actually change how this capital moves or just relabel it.

Private credit has become one of the loudest stories in finance over the past few years, a roughly $1.5 trillion market that grew up in the gap left by banks pulling back from mid-market lending. Now a company called Trad.Fi wants to move a slice of it onto blockchain rails. The firm announced plans to bring $650 million in private credit on-chain and named W3.io as the infrastructure partner handling the capital workflows behind it.

The problem Trad.Fi is going after

Private credit is profitable and opaque in equal measure. Loans are negotiated bilaterally, documented in PDFs, and serviced through a patchwork of spreadsheets, custodians, and administrators. Once a deal closes, an investor's position is hard to see, harder to value between reporting periods, and nearly impossible to trade without a slow secondary process. That friction is the point for some incumbents, since opacity supports fees, but it also caps who can participate and how quickly capital can be redeployed.

Trad.Fi's pitch is that tokenizing these credit positions makes them legible. If a loan and its repayment schedule live on-chain as a programmable instrument, servicing events, interest accruals, and ownership transfers become entries anyone with permission can verify in real time. The $650 million figure is the company's stated near-term pipeline rather than assets already converted, which is a distinction worth holding onto. Announced pipelines in tokenized real-world assets have a long history of arriving later and smaller than the press release suggests.

Where W3.io fits

The more revealing part of the announcement is the choice to outsource the hard part. Trad.Fi is not building its own settlement and lifecycle engine. It is taking W3.io to power what both companies describe as capital workflows, meaning the orchestration of subscriptions, redemptions, interest distributions, and compliance checks that a credit fund runs continuously.

This is the layer that usually breaks tokenization projects. Minting a token to represent a loan is trivial. Keeping that token synchronized with a legal claim, enforcing transfer restrictions so only qualified investors hold it, handling KYC and accreditation, and pushing cash flows to holders on schedule is operations-heavy work that sits between smart contracts and regulated off-chain entities. By renting that infrastructure rather than building it, Trad.Fi can focus on origination and investor relationships, the parts where a credit shop actually earns its keep.

Why the on-chain angle matters, and where to stay skeptical

The case for putting private credit on-chain rests on a few concrete improvements. Settlement that takes days through traditional administrators can compress to minutes. A position that is effectively frozen until maturity could trade on a secondary market if enough buyers and a compliant venue exist. Reporting that arrives quarterly in a PDF could become a live feed. For institutional allocators managing exposure across dozens of credit funds, that visibility has real value.

The case for caution is equally concrete. Tokenization does not improve the underlying loans. A $650 million book of private credit carries the same default risk, the same covenant quality, and the same recovery uncertainty whether it sits in a database or on a blockchain. Liquidity also remains a promise rather than a feature until trading volume materializes, and most tokenized credit products to date have thin or nonexistent secondary markets. The legal enforceability of an on-chain claim still depends on off-chain contracts and the jurisdiction governing them, so the token is a representation, not the asset itself.

There is also the structural question of who benefits. Faster settlement and transparent reporting are genuinely useful to investors. They are less obviously useful to the managers who have built businesses on the existing frictions. Projects that succeed in this category tend to be the ones aligning the operational upside with the people who control deal flow, and that alignment is hard to read from a launch announcement.

The broader pattern

Trad.Fi is moving into a space that has drawn serious institutional names. Established asset managers have tokenized money market funds and Treasury products, and several platforms are racing to do the same for private credit specifically, since it combines high yield with a desperate need for better infrastructure. The competition is less about technology, which is increasingly commoditized through providers like W3.io, and more about who can source quality loans and convince allocators to hold a tokenized wrapper instead of a familiar fund structure.

For Trad.Fi, the partnership model is a reasonable bet. It lets a smaller player ship faster by standing on shared infrastructure, and it concentrates the company's effort on origination. The measure of whether this works will not be the $650 million headline. It will be how much of that pipeline actually converts, whether the tokenized positions trade or simply sit, and whether investors get reporting and liquidity they could not have gotten through a conventional fund. Those answers come quarters from now, not at launch.

Comments

Please log in or register to join the discussion