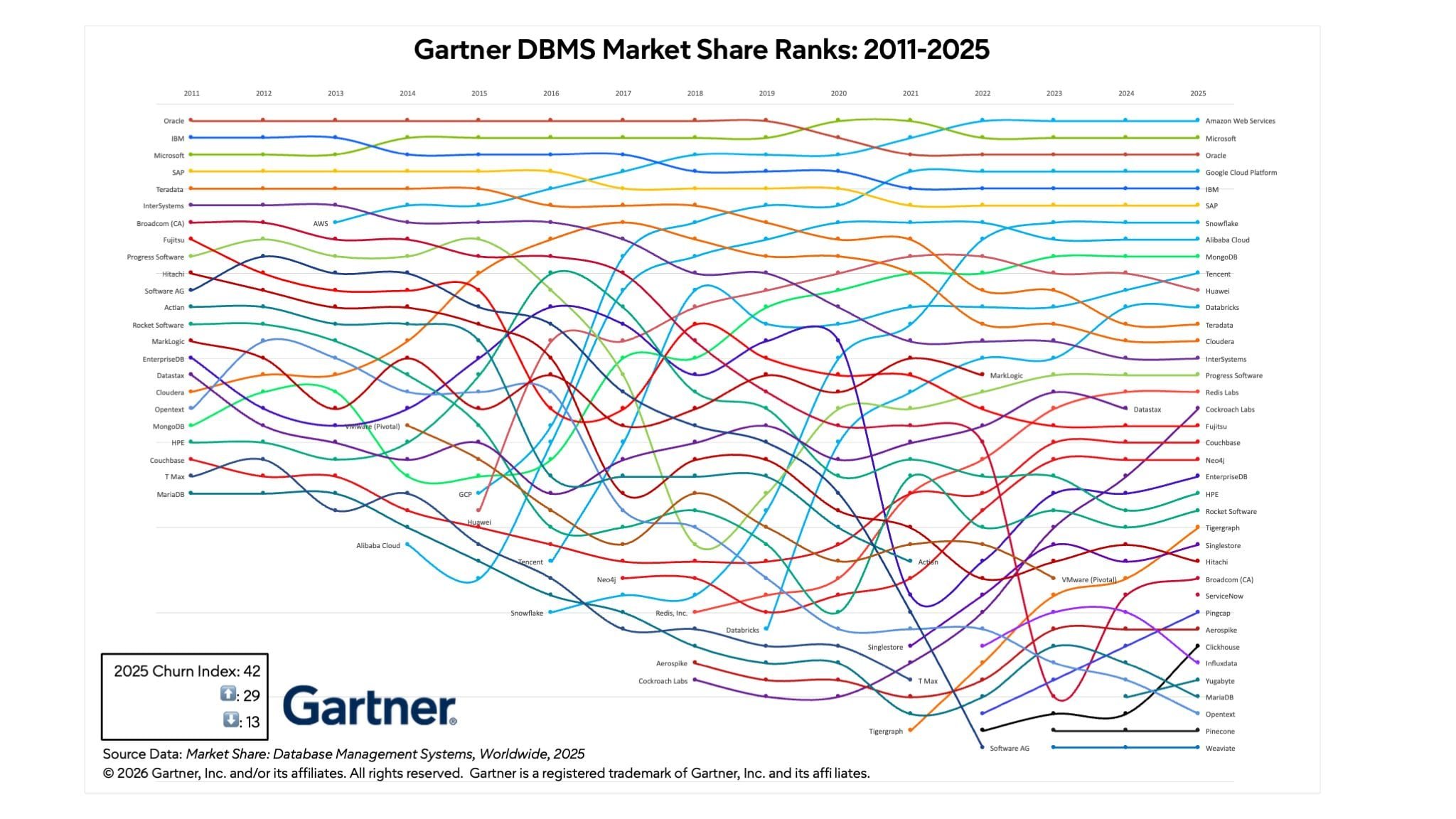

Gartner's 2025 DBMS Market Share Ranks shows Oracle losing ground to cloud providers and emerging databases, with Microsoft as the only legacy vendor gaining share since 2011.

The database market is undergoing a fundamental shift that's been years in the making, and Gartner's latest DBMS Market Share Ranks: 2011-2025 visualization makes it crystal clear: Oracle's once-unassailable dominance is slowly eroding.

The chart itself resembles a chaotic subway map, but the message is unmistakable. While the top five vendors (AWS, Microsoft, Oracle, Google Cloud Platform, and IBM) have remained stable since 2022, the long-term trend tells a different story.

The slow decline of database incumbents

According to Adam Ronthal, vice president analyst at Gartner, the data reveals a stark reality: "Of the leading vendors in 2011 (Oracle, IBM, Microsoft, and SAP), only Microsoft has grown their market share in the last 15 years. The others have ceded market share to Amazon, Google Cloud Platform, and a handful of smaller but emerging vendors like Snowflake, Databricks, and MongoDB."

This isn't a sudden collapse but rather a gradual redistribution of market power. The database landscape that Oracle once dominated is fragmenting into specialized services and cloud-native solutions.

Cloud, analytics, and AI drive market evolution

The primary growth drivers in 2025 remain consistent with recent years: cloud adoption, analytics workloads, and artificial intelligence applications. Ronthal notes that "leading vendors are adapting well to the demands of AI and cloud," which explains the relative stability at the top of the market.

However, the "churn" in the lower half of the rankings tells an equally important story. Here, smaller vendors can make significant moves with individual large deals, and users are actively seeking differentiated offerings from up-and-coming providers.

The meteoric rise of Cockroach Labs exemplifies this trend. The company behind CockroachDB, which combines a PostgreSQL-like interface with distributed architecture, continues its dramatic ascent in the rankings.

Oracle's strategic crossroads

Oracle occupies a unique position in the database ecosystem. For organizations with existing Oracle deployments, the calculus is straightforward: replacing a comprehensive Oracle setup would be prohibitively expensive and risky. A CIO attempting to eliminate "wall-to-wall Oracle" infrastructure would likely face significant career consequences.

Conversely, organizations building new, cloud-native applications have different priorities. Oracle may not be their first choice, particularly when mature open-source alternatives like PostgreSQL are available as cloud services on AWS, Azure, and Google Cloud.

Oracle's cloud strategy compounds this challenge. While Oracle Cloud Infrastructure (OCI) positions itself as a platform for new application development, Oracle's market share in cloud infrastructure remains tiny compared to the top three providers. The company largely relies on its enterprise application dominance to drive cloud adoption rather than competing on cloud infrastructure merits alone.

The open-source factor

Gartner's revenue-based measurements exclude pure open-source database systems, but other metrics paint a complementary picture. DB-Engines, which tracks website mentions, search trends, technical discussions, and job postings, shows PostgreSQL steadily climbing toward third place, potentially overtaking SQL Server.

Among developers, PostgreSQL became the most popular database in 2023 according to StackOverflow rankings, while Oracle sits in ninth place. This developer preference signals where the market may be heading as new applications are built and old ones are retired.

What this means for the future

The trend lines are clear: Oracle's market share will likely continue to decline gradually. However, this doesn't spell immediate crisis for the company or for Oracle database professionals.

Ronthal emphasizes that "the relatively stable stack ranks at the top half of the market indicate that leading vendors are adapting well to the demands of AI and cloud." Users remain committed to their strategic investments while exploring new options.

For newly-qualified Oracle DBAs, the career outlook remains positive for the foreseeable future. The "long tail" of Oracle deployments ensures ongoing demand for expertise. However, the company's strategic priorities increasingly focus on AI infrastructure rather than database market share preservation.

The database market's evolution reflects broader technological shifts: the move to cloud, the rise of specialized data platforms, and the growing importance of developer experience. Oracle's gradual decline isn't a failure but rather the natural consequence of a market that has fundamentally changed since the company's period of dominance.

As organizations continue to modernize their technology stacks, the database landscape will likely become even more diverse, with cloud providers, specialized vendors, and open-source solutions all playing significant roles. Oracle will remain a major player, but its era of unquestioned dominance appears to be drawing to a close.

Comments

Please log in or register to join the discussion