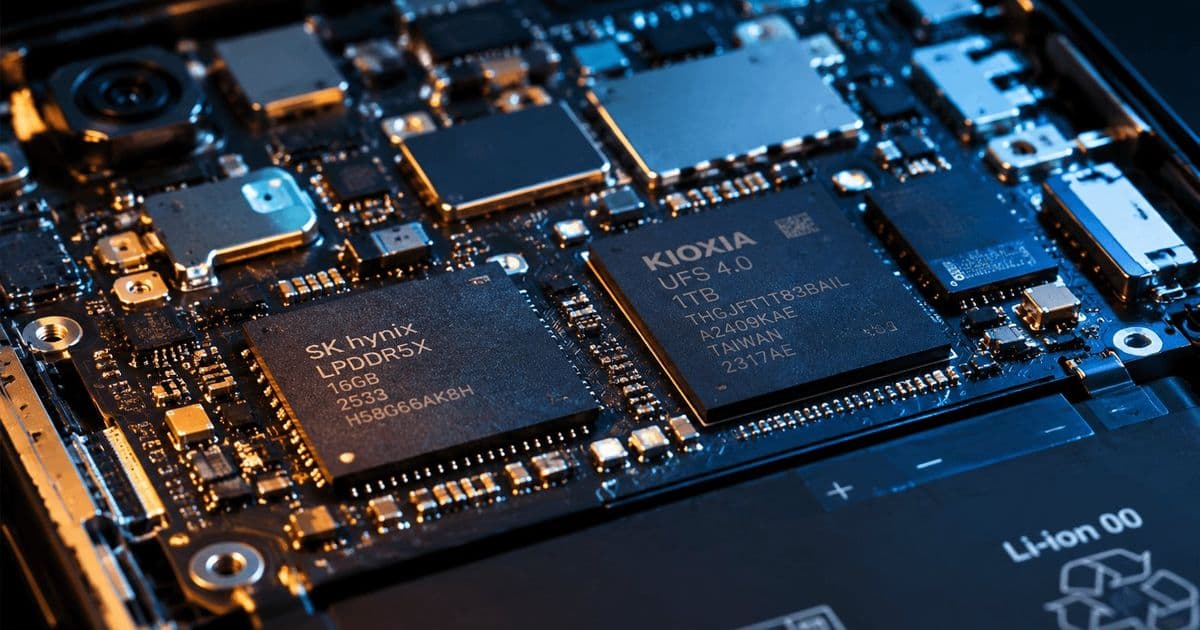

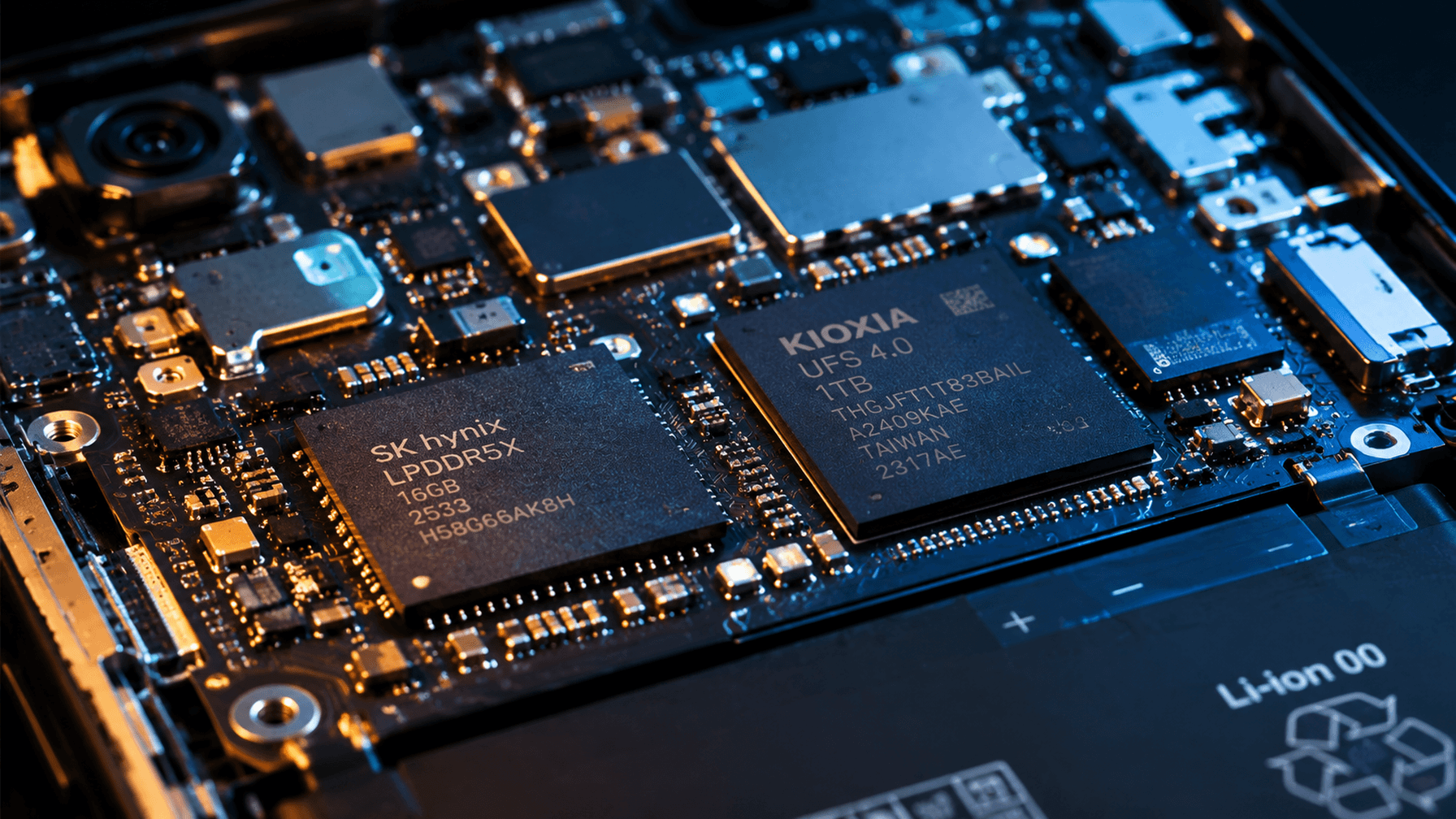

DRAM and NAND prices have spiked 40-90% in recent quarters, driven by AI infrastructure demand and supply constraints. Chinese smartphone manufacturers are now reverting entry-level devices from 12GB to 6GB RAM, reversing years of spec progression.

The smartphone industry's steady march toward higher memory specifications has hit a wall. After years of incremental upgrades where budget phones moved from 4GB to 8GB to 12GB of RAM as standard, manufacturers are now pulling back to configurations not seen since 2022.

According to data from TrendForce, DRAM contract prices have risen over 40% for two consecutive quarters spanning Q4 2025 through Q1 2026. Counterpoint Research reports even more dramatic increases, with all memory categories posting 80-90% sequential price jumps in Q1 2026 alone. DRAM, NAND flash, and HBM chips have all hit record highs simultaneously, an unprecedented convergence that has caught the industry off guard.

What's Actually Happening

Chinese smartphone manufacturers including Xiaomi are redesigning their entry-level lineups. Budget devices that had standardized on 12GB RAM and 256GB storage are being reconfigured with 6GB RAM and 128GB storage. The display situation is equally grim, with makers reverting to 1080p LCD panels and older notch designs to maintain price points.

Mid-range devices face the most acute pressure. Manufacturers must choose between raising retail prices or cutting specifications across multiple components to offset memory costs. Neither option is palatable in a market where consumers have grown accustomed to consistent spec improvements at stable or declining prices.

Xiaomi founder and CEO Lei Jun publicly called the price increases "crazy" on social media, advising consumers to purchase devices sooner rather than later. He indicated the rally may persist for two more years, a timeline that aligns with analyst projections.

Why This Is Happening

The memory price surge stems from three converging factors:

AI infrastructure demand. The buildout of AI training and inference capacity has consumed enormous quantities of HBM (High Bandwidth Memory) and high-capacity DRAM. Nvidia's latest GPUs require multiple HBM stacks, and every new AI data center deployment draws from the same fabrication capacity that supplies consumer electronics. This demand shows no signs of abating as hyperscalers continue expanding.

NAND supply constraints. Industry consolidation has reduced the number of NAND flash manufacturers, limiting supply flexibility. When demand spikes, there are fewer competitors who can ramp production quickly. The 2024 destocking cycle also left manufacturers with lean inventories, and the subsequent restocking phase has amplified price pressure.

Capacity discipline. Memory makers learned from previous boom-bust cycles. Instead of aggressive capacity expansion that previously led to price crashes, manufacturers are maintaining disciplined production growth. This benefits their margins but constrains the supply response that might otherwise moderate price increases.

What This Means For Consumers

The immediate impact is straightforward: fewer upgrades for the same money, or the same specifications at higher prices. But the secondary effects matter more.

The spec regression creates a fragmented ecosystem. App developers who had begun optimizing for 12GB+ RAM environments will need to reconsider memory footprints. Features like aggressive background app caching, on-device AI processing, and high-resolution camera computational photography all depend on available memory.

For the broader market, this represents a check on the assumption that consumer electronics specs improve linearly over time. Memory is a commodity subject to the same supply-demand dynamics as oil or wheat. When a new demand vector (AI infrastructure) competes for the same fabrication capacity, consumer products absorb the shock.

Limitations and Context

The current situation is not without nuance. The price data from TrendForce and Counterpoint reflects contract prices, which can diverge from retail pricing as manufacturers absorb costs or adjust margins. Some of the spec downgrades may also reflect strategic decisions to differentiate product tiers more aggressively, rather than purely cost-driven necessity.

Additionally, the 80-90% sequential increases reported by Counterpoint represent quarter-over-quarter changes during an unusual period. Annual price comparisons, while still showing significant increases, present a less dramatic picture.

The timeline for resolution remains uncertain. If AI infrastructure demand moderates or memory makers accelerate capacity expansion, prices could stabilize sooner than Lei Jun's two-year forecast suggests. But given the structural factors at play, a return to 2024 pricing levels appears unlikely in the near term.

For now, the smartphone industry's spec trajectory has been reset by forces outside its control. The memory market's cyclical nature has reasserted itself, this time amplified by the AI buildout. Consumers and manufacturers alike will need to adapt to a new baseline.

Comments

Please log in or register to join the discussion