This article traces the 1040's journey from its 1913 debut targeting the wealthy to its WWII expansion to ordinary citizens, examining early filing struggles, technological evolution from TeleFile to COBOL systems, and why the form remains a cultural touchstone despite decades of reform attempts.

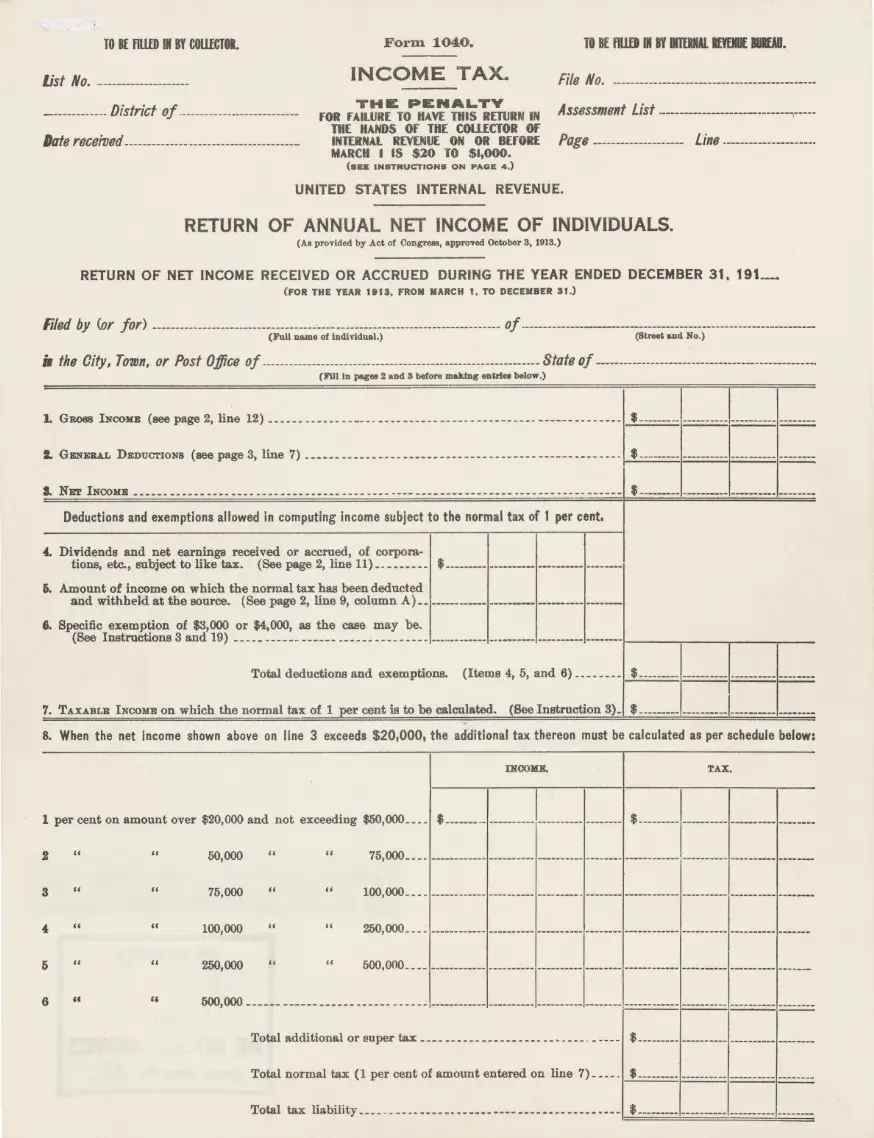

The very first Form 1040, introduced in 1913, was a stark two-page document designed for a nation where income taxation was still a novel concept. Ratified alongside the Sixteenth Amendment, it arrived in a America where most citizens had never interacted with federal income tax—a system initially conceived to fund the Civil War but struck down as unconstitutional in 1895. The amendment’s passage changed that, though early thresholds meant only those earning over $3,000 annually (roughly $100,000 today) needed to file. For the fortunate few who did, January 1914 brought confusion: blanks for January and February appeared on forms meant for income earned after March 1913, prompting New York Times readers to question why the IRS hadn’t adjusted for the timing gap.

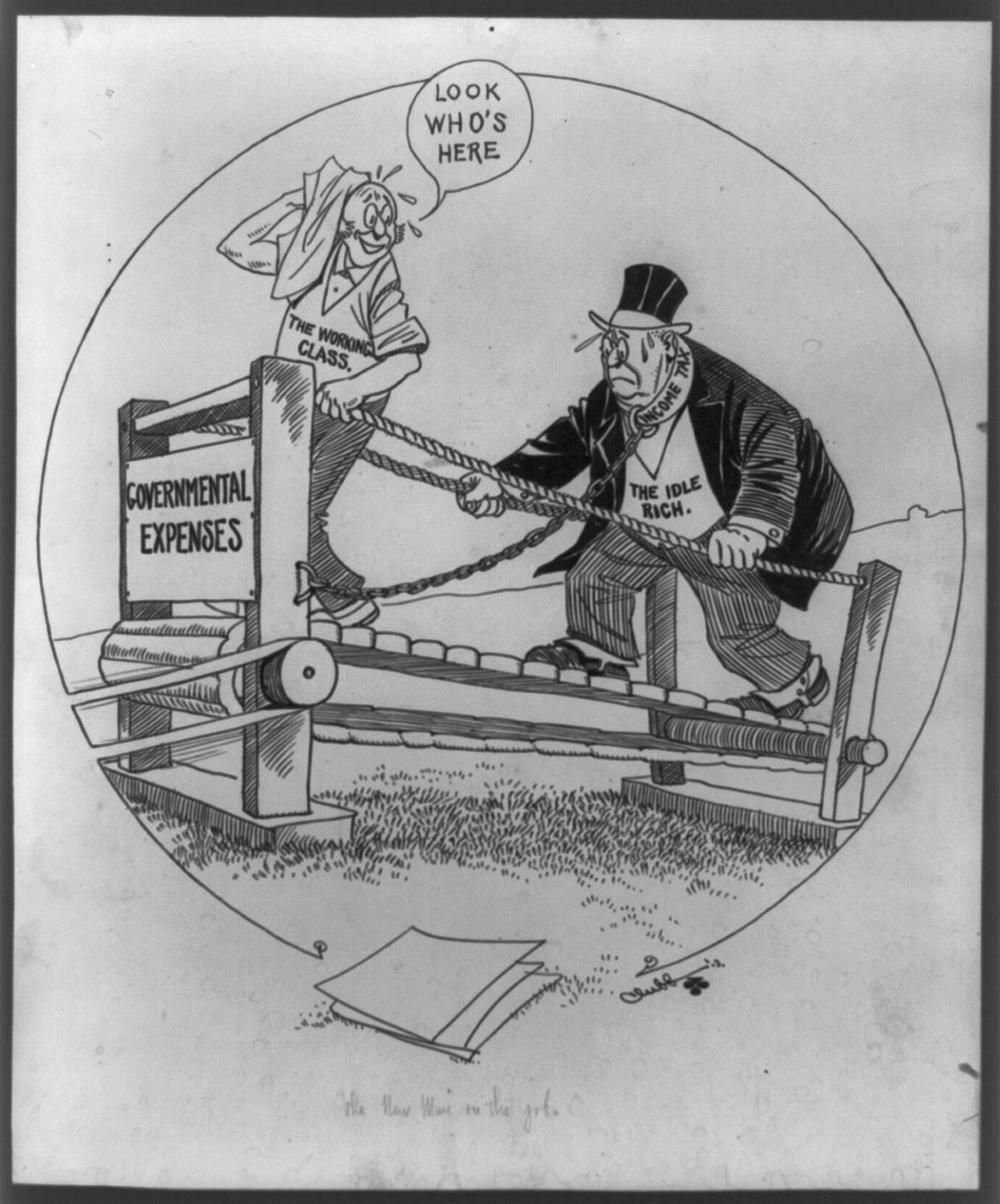

Filing required more than arithmetic—it demanded cultural translation. Financial editor B.C. Forbes, later founder of the eponymous magazine, urged readers in Hearst’s New York American to view compliance through dual lenses: patriotism and fear of penalties ranging from $20 fines to imprisonment. His warning echoed in editorial cartoons like John Scott Chubb’s “The New Man on the Job,” which gained resonance as World War I pushed marginal rates above 70% for the ultra-wealthy. Yet even then, the system remained a rich person’s burden—a fact critics of modern taxation often cite when arguing against progressive rates, overlooking that mass participation came decades later.

That shift arrived with World War II. The Revenue Act of 1942 dramatically lowered income thresholds, pulling millions of salaried workers into the 1040 ecosystem overnight. Suddenly, the IRS faced a crisis of scale: its existing quarterly/annual payment model assumed financially savvy taxpayers, not factory workers juggling rent and ration books. Enter Beardsley Ruml, Macy’s economist, who convinced Congress to adopt “pay as you go” via the Current Tax Payment Act of 1943. By embedding tax collection in payroll deductions, Ruml solved the immediacy problem—though the transition included a one-time 75% tax cut for 1943, framed by contemporary analysts as an introductory offer to ease the shock.

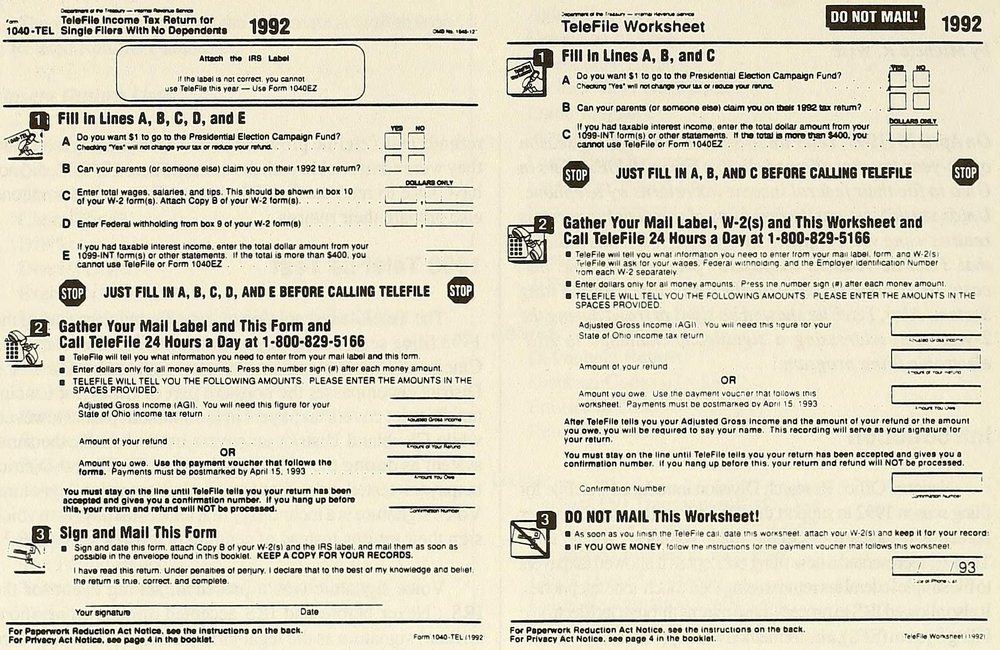

The mid-century era also birthed experiments in accessibility. Rodman L. Modra’s magazine-length tax guide, discovered decades later in a junk store, promised 500 questions and answers with workbook-style income trackers—a proto-TurboTax for the pen-and-paper set. Around the same time, the IRS launched TeleFile in 1992, letting filers submit returns via touch-tone phone using worksheet codes. Though innovative, it highlighted a persistent tension: the IRS’s embrace of new tools (it was an early PDF adopter in 1994) often outpaced its ability to retire legacy systems. The Individual Master File, built on COBOL and assembly language in the 1960s, still underpins core operations—a 2023 GAO report estimates full modernization won’t occur until 2030, leaving known security vulnerabilities unaddressed for years.

Today’s tax software industry, valued in billions, exists partly because the 1040 remains fundamentally opaque to the average filer. Yet historical guides like Modra’s remind us that complexity isn’t inherent—it’s a product of accumulated exemptions, credits, and shifting political compromises. The free-file debate, reignited periodically by advocates like Elizabeth Warren, echoes Ruml’s original insight: taxation need not be a yearly ordeal if systems prioritize user agency over institutional inertia. As we navigate another filing season, the 1040’s endurance isn’t just about revenue—it’s a ledger of how America balances civic duty with the practical realities of making compliance possible for everyone, not just those who can afford help.

Comments

Please log in or register to join the discussion